Key Points

- Most subscription businesses measure failed payments asa transaction metric. The actual cost is an LTV loss — and those two numbers are not close to each other.

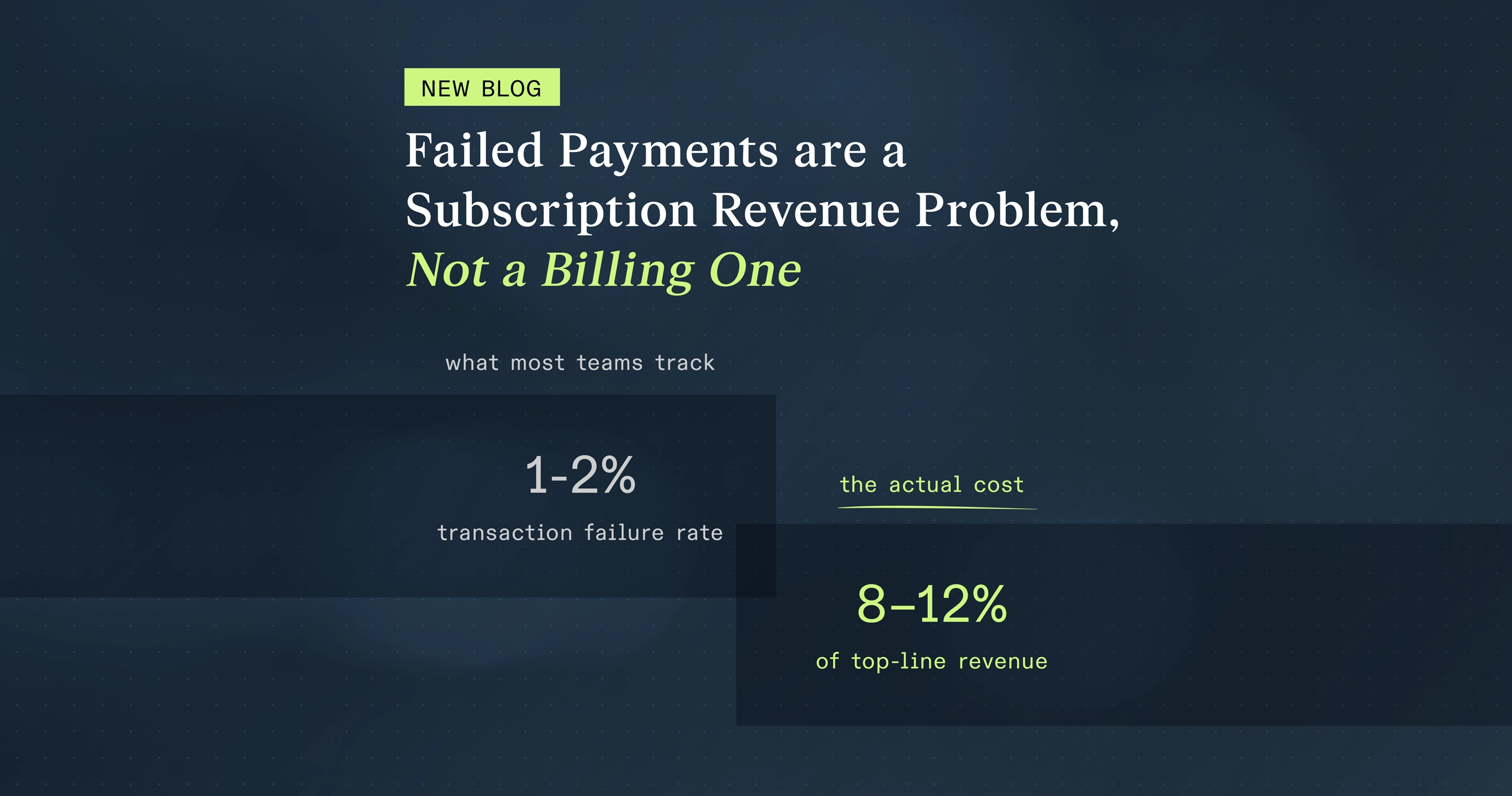

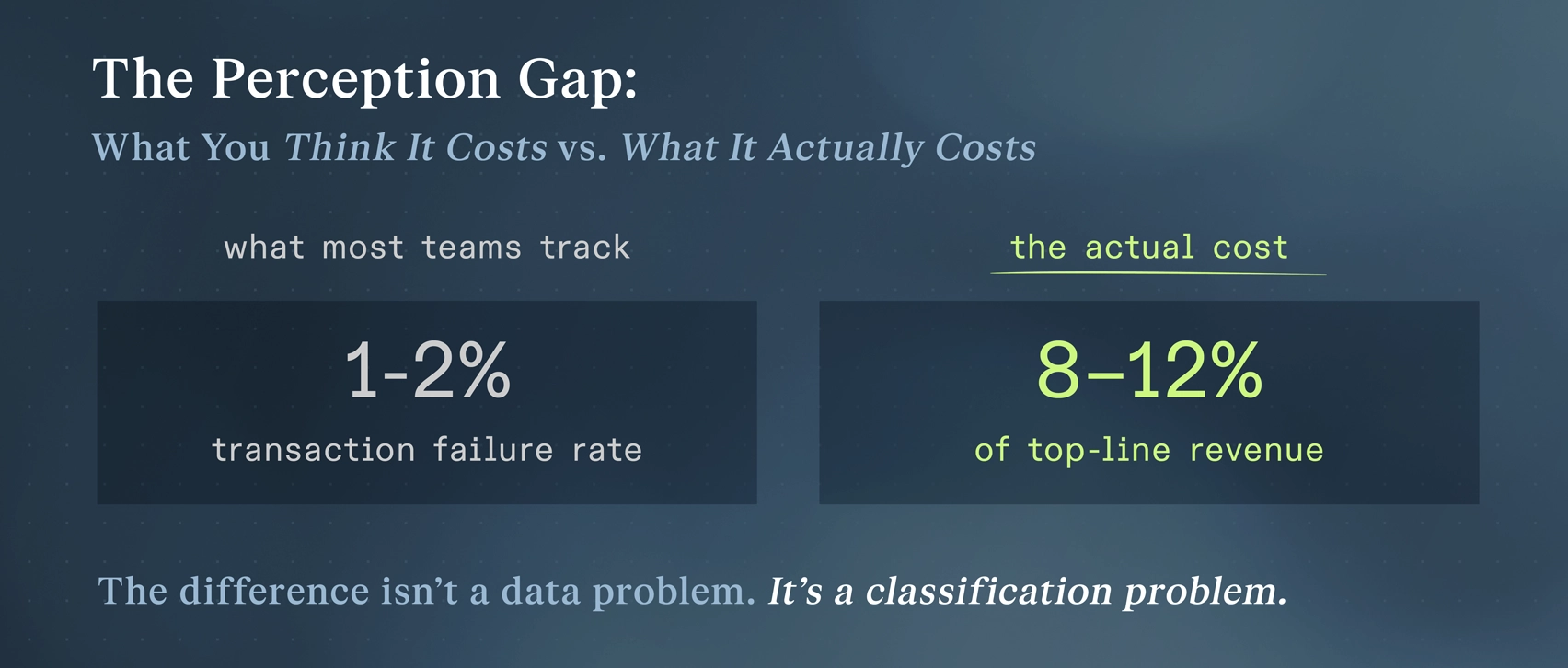

- Industry research puts the true cost of failed payments at 8–12% of top-line revenue. Most finance and revenue teams assume it’s 1–2%.

- Approximately two-thirds of failed subscription payments are false declines — legitimate transactions the issuing bank turned down anyway. The average monthly decline rate for recurring billing is 24%.

- Standard dunning and recovery communications don’t just underperform — they can actively accelerate churn by placing customers at an unplanned cancellation decision point.

- The highest-performing recovery programs operate entirely within the payments infrastructure — recovering revenue without the customer ever knowing a payment failed.

There is a number on your P&L that is almost certainly wrong — the one associated to failed payments

At some point in the last quarter, you looked at a churn number that didn't quite make sense. Your retention programs are running. Your product hasn't meaningfully degraded. Voluntary cancellations are within range. But the revenue forecast still has a gap, and the explanation isn't obvious.

For most subscription businesses, a significant portion of that gap traces back to failed payments — and to the fact that failed payments are being measured as a billing problem when theircost is a revenue one.

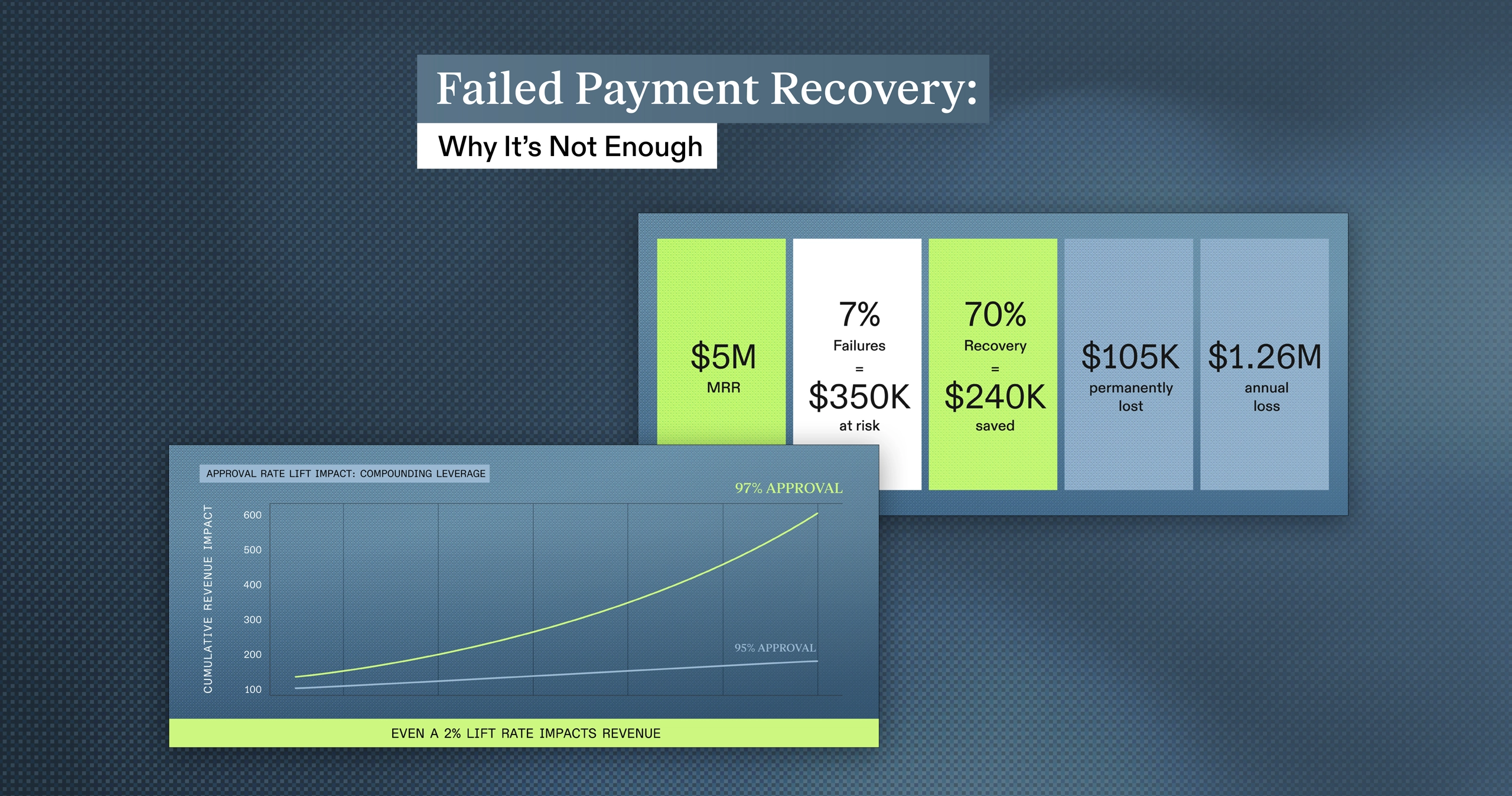

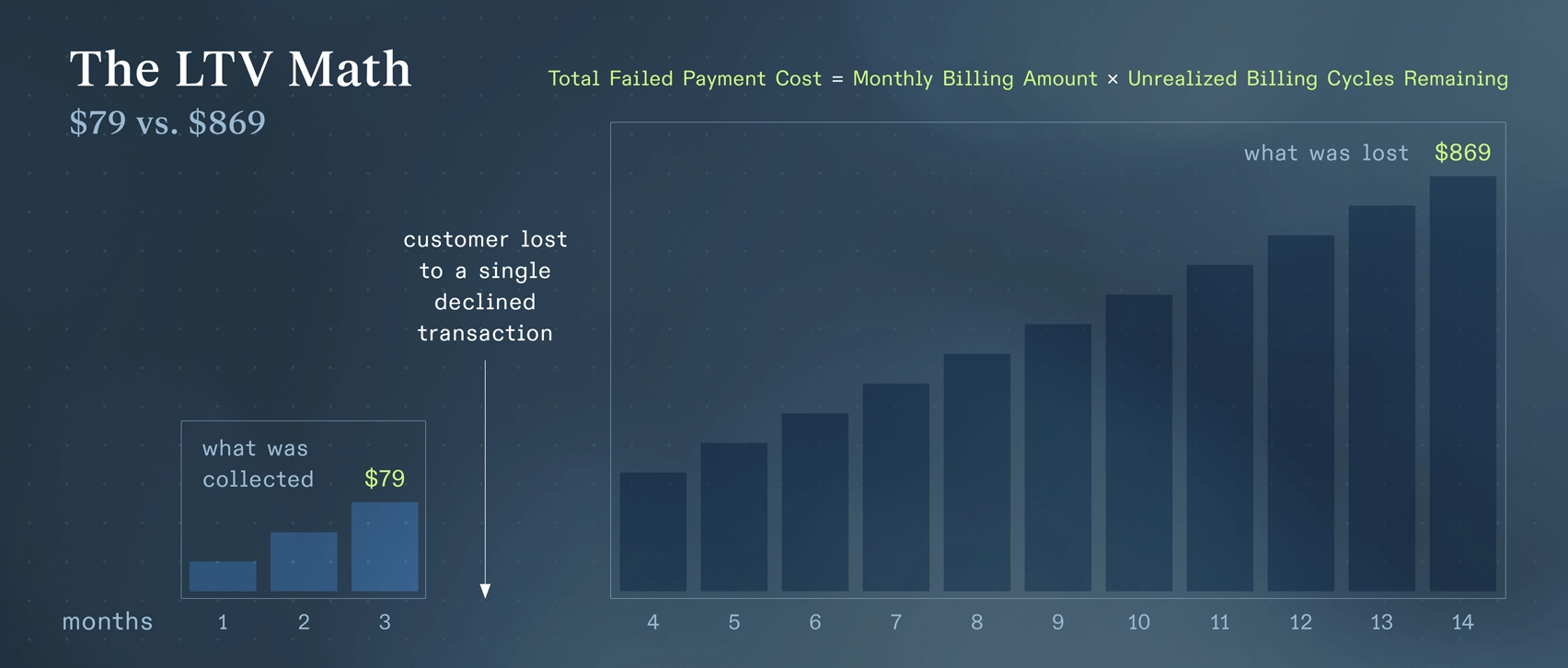

Here’s the calculation that makes this real. If your business bills customers $79 per month and the average customer stays for 14 months, a failed payment in month three does not cost $79. It costs $79 multiplied by the 11 billing cycles that customer would have completed: $869 in lost revenue from a single declined transaction. Scale that across every unrecovered failed payment in a month and the number looks very different from what appears in your payment processor report.

Industry research puts true failed payment rates for subscription businesses between 8% and 12% of top-line revenue. Most finance and revenue leaders believe the number is 1–2%. The difference is not a data problem— it’s a classification problem. Failed payments produce an LTV loss, but they’re being tracked in a system designed to count transactions.

Total Failed Payment Cost = Monthly Billing Amount × Unrealized Billing Cycles Remaining

We’ll explain where the gap comes from, how to calculate your actual exposure, and what changes when you move the problem from the billing queue to the P&L.

Why Subscription Businesses Underestimate Failed Payment Costs

Most subscription businesses track failed payments as a transaction metric: the percentage of billing attempts that failed in a given month. That number is real. But a failed payment is not a missed transaction — it is a potential customer loss. The moment a subscription lapses because of a declined card and is not recovered, the business does not lose one month of revenue. It loses every billing cycle that customer would have generated from that point forward.

The second reason the estimate persists is structural. Revenue teams work in MRR dashboards. Finance teams work in cash flow reports. But neither system is designed to connect payment failure rates to customer lifetime value in a way that makes the full cost visible. The gap does not persist because anyone is hiding it— it persists because nobody's reporting setup is built to show it.

Most subscription businesses track failed payments as a transaction failure rate. The actual cost is calculated at the LTV level — and those two numbers look completely different.

What Is Actually Declining — And Why It Matters

Not all failed payments carry the same cost or the same cause. Understanding the difference is essential to measuring your actual exposure and to knowing where to focus.

Hard Declines

Hard declines are definitiverejections: an expired card, a cancelled account, an invalid number. The card itself is the problem. Recovery requires the customer to actively update their payment information, which introduces a separate risk category addressed below.

Soft Declines (Temporary False Declines)

Soft declines are the more consequential and more misunderstood category. A soft decline is a rejection where the card is valid, the customer has credit, and the customer wants to pay— but the issuing bank's authorization system said no anyway.

This type of false decline can also occur when a bank or payment processor incorrectly rejects a legitimate credit card transaction, mistakenly flagging it as fraudulent. These occur due to overly strict fraud filters, as well as atypical spending patterns, address mismatches, or high-risk transaction flags, causing valid purchases to be declined. According to Visa, they account for approximately two-thirds of all failed payments in subscription billing, and the average monthly decline rate across recurring billing transactions is 24%.

The reason false declines are so prevalent in subscription billing is structural. Recurring transactions are automated, not cardholder initiated. They process without the cardholder's active involvement at the moment of billing, a condition known as Card-Not-Present (CNP). These characteristics systematically increase the risk score issuing bank algorithms assign — even when the underlying transaction is entirely legitimate.

Banks are not acting irrationally.They absorbed $179 billion in direct fraud losses in 2025 and need to catch fraudulent transactions in milliseconds. Their models are calibrated to minimize their own losses because approving a fraudulent transaction creates a direct cost for the bank.

For a one-time e-commerce purchase, a false decline means a frustrated customer who tries a different card. For subscription billing, an unresolved false decline produces a churned customer who might never come back.

The Second Wave: Churn You Trigger Yourself

There's a second cost category embedded in failed payment programs that most people miss entirely: well-intentioned recovery methods can create more churn.

When a customer's payment fails, the standard response is to tell them. A dunning email goes out. Service isinterrupted. The customer is asked to update their payment information to continue their subscription. These actions do recover some revenue, so they seem like the right thing to do.

But a failed payment notification does more than prompt a card update. It asks the customer to solve a problem they did not create, it associates the brand with a billing issue, and it places the customer at an unplanned decision point: is this subscription worth the friction of acting on it right now?

Customers who were on the fence about their subscription and might not have cancelled will sometimes decide to end the relationship when you contact them about their failed payment. The dunning communication handed them a natural exit and they took it.

This second-wave churn is real and itis measurable — but it rarely surfaces in failed payment analyses because the customer is recorded as a dunning non-responder rather than a payment-triggered cancellation. The recovery logic looks like it failed, but in reality, it was the communication itself that accelerated the churn.

The highest-performing recovery approaches operate entirely within the payments infrastructure, without requiring customer-facing communication unless no other option exists. The customer who never knows their payment failed has no reason to reconsider their subscription.

How to Calculate Your Actual Exposure

Here’s how to build a working estimate from data you already have.

Step 1: Pull Your Gross Failed Payment Rate

Pull six months of billing data from your payment processor. Calculate the percentage of billing attempts that resulted in a decline — including declines your retry logic eventually resolved, not just the ones that went unrecovered. This is your gross failed payment rate.

Most businesses find this number is meaningfully higher than the net failure rate reported in their subscription management dashboard. The difference between gross and net is what your current dunning or retry logic is catching.

Step 2: Isolate Involuntary Churn

In your churn data for the same period, identify churned customers who had a failed payment in the 30 days before their cancellation or lapse date. This gives you a working population of involuntary churners. It will not be perfectly precise, but it will be directionally accurate — and directional accuracy is enough to size the opportunity.

Step 3: Apply the LTV Multiplier

For the involuntary churn population,calculate how many billing cycles each customer would have completed had they remained active to your average customer lifespan. Multiply by their monthly billing amount. Sum across the cohort. This is your monthly involuntary churn LTV cost.

The three inputs you need:

- Churned customers in the past 6 months

- Customers who had a failed payment in the 30 days before churning

- Average customer lifespan in billing cycles

Step 4: Annualize and Stress-Test

Multiply your monthly LTV cost figure by 12. Then model recovery scenarios: what is the revenue impact if you recover 30% of those customers? 50%? 70%? This range produces the business case for investment in payment performance improvement, stated in terms a CFO can evaluate directly.

Step 5: Identify What Is in the Gap

Compare your gross failed payment rate to your net unrecovered rate. The difference is what your current retry logic is capturing. The remaining unrecovered volume — especially the portion attributable to false declines on legitimate customers — is your opportunity.

What Better Performance Actually Looks Like

For subscription businesses that run this math and find a number worth addressing, the question is: how do you fix the problem?

Basic retry logic — reattempting a declined transaction on a fixed schedule — captures some recoveries. But it treats every failed payment the same way, and failed payments are not uniform.The issuing bank, the decline reason code, the card type, the customer's billing history, and the timing of the retry all affect the success of another attempt. A one-size-fits-all retry schedule leaves significant recovery on the floor.

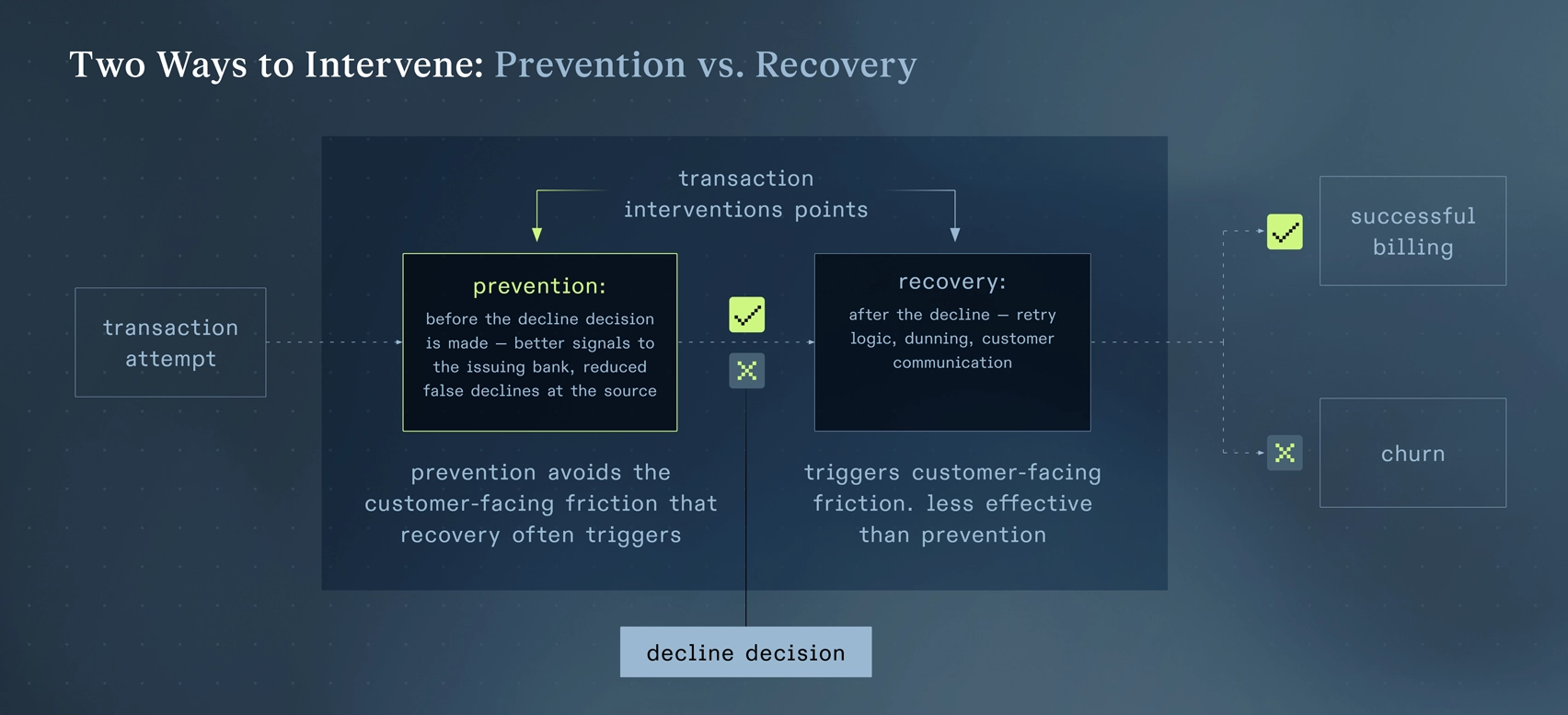

The more significant distinction is where in the payment lifecycle you intervene.

Most recovery tools operate after the decline. They retry the transaction, send dunning communications, and ask customers to take action. These methods recover revenue in cases they reach,but they accept the decline as a given and work around it from there. They are also the methods most likely to trigger the second-wave churn described earlier.

A prevention-first approach operates upstream. By establishing data relationships directly with issuing banks, it’s possible to give authorization systems better signals before the decline decision is made — reducing false declines at the source rather than recovering them afterward. For subscription businesses, fewer false declines means fewer customers entering the recovery funnel and fewer customers receiving the communications that can trigger cancellation.

Recovery still matters for the declines that do occur. But the highest-performing programs treat prevention and recovery as two distinct levers, and they prioritize the one that does not require telling your customer anything went wrong.

The metrics that matter:

- Recovery rate — the percentage of failed payments successfully recovered

- Post-recovery customer lifespan— how long recovered customers remain active compared to the baseline average

- Customer-facing friction — whether recovery methods create service interruptions or dunning touchpoints that can accelerate cancellation

- LTV of recovered customers— the total revenue earned over the customer's remaining subscription life, not just the single recovered payment

The Number Worth Knowing

That 8–12% figure we mentioned earlier is not a ceiling — some companies have even higher failed payment rates. And the gap between their perceived lost revenue — that 1-2% — and their actual lost revenue is large enough to justify treating payment performance as a revenue priority, not a billing operations line item. In other words, it hurts enough to do something about it.

Revaly works with subscription and recurring billing businesses to quantify failed payment exposure and improve performance at two layers: the authorization layer— where false declines can be reduced by up to 50% — and the recovery layer —where intelligent retry logic captures revenue without customer-facing friction. Contact us to start the conversation.

What to bring to that conversation:

- Your gross failed payment rate from your Payment Service Provider

- Your average customer lifespan in billing cycles

- Your average monthly billing amount

- Your current retry or recovery approach

With those four inputs, Revaly can build a baseline estimate of your current LTV exposure and what meaningful improvement in payment performance would be worth to your business.