Consider what it means when a two-year customer — someone who auto-renews without hesitation and has never once disputed a charge — has their payment incorrectly rejected. Their card is valid, their account is in good standing, and they have no idea anything is wrong until they receive a generic decline message that offers no explanation. That moment, unremarkable from a system standpoint, is often where the relationship ends.

This scenario plays out millions of times a day. The scale of the problem is staggering: according to research analyzed by Sci-Tech Today, false declines — where valid transactions from legitimate customers are incorrectly rejected — cost businesses an estimated $308 billion globally in 2023 alone. That figure dwarfs actual fraud losses by a significant margin. And the kicker is that up to 70% of declined e-commerce orders are from real, creditworthy customers, according to research cited by Kipp.

What makes this loss so damaging is not just the immediate missed transaction — it's the ripple effect. A Sapio Research survey found that 33% of U.S. consumers say they will never shop again with a merchant that falsely declines their order. And per PYMNTS and FlexPay research, declined card payments account for 50% of all customer churn in subscription businesses, meaning half of the people walking out the door were never trying to leave.

The problem is not that payments fail. Payments fail for reasons that range from the technical to the systemic to the genuinely unavoidable. The problem is that most merchants have never examined the root causes of those failures, have not built infrastructure to prevent them, and continue to manage approval rates as an afterthought rather than a strategic lever. This post breaks down the real,controllable drivers of higher approval rates and explains why so many merchants are leaving this opportunity on the table.

Why Most Merchants Get Approval Rates Wrong

Before getting into what drives higher approval rates, it is worth understanding the mindset that holds most merchants back. The dominant posture in payments today is reactive: when a payment fails, send a dunning email, queue a retry, follow up with the customer. This approach treats the decline as the end of the story— a cleanup operation — rather than as a symptom of an upstream problem that could have been avoided.

That reactive posture is expensive in ways that rarely appear on a dashboard. Research from Harvard Business Review, citing Bain & Company, consistently finds that acquiring a new customer costs anywhere from five to 25 times more than retaining an existing one. The probability of successfully selling to anew customer is 5 to 20%, while the probability of selling to an existing one is 60 to 70%. When a legitimate payment fails and a customer churns as a result, you are not just losing one transaction, you are losing the full lifetime value of that relationship and paying again to replace it.

There is also a measurement problem that compounds this. Most merchants track authorization rates as their primary payment KPI: the ratio of authorization attempts approved by card issuers. Authorization rate is the right thing totrack, but most merchants aren’t looking at what’s actually driving it, so the results can be confusing. When a payment fails and your system initiates recovery retries, each retry counts as a new authorization attempt, which means your reported authorization rate can actually fall even as you are recovering more revenue. The metric appears to be punishing you for doing your job well.

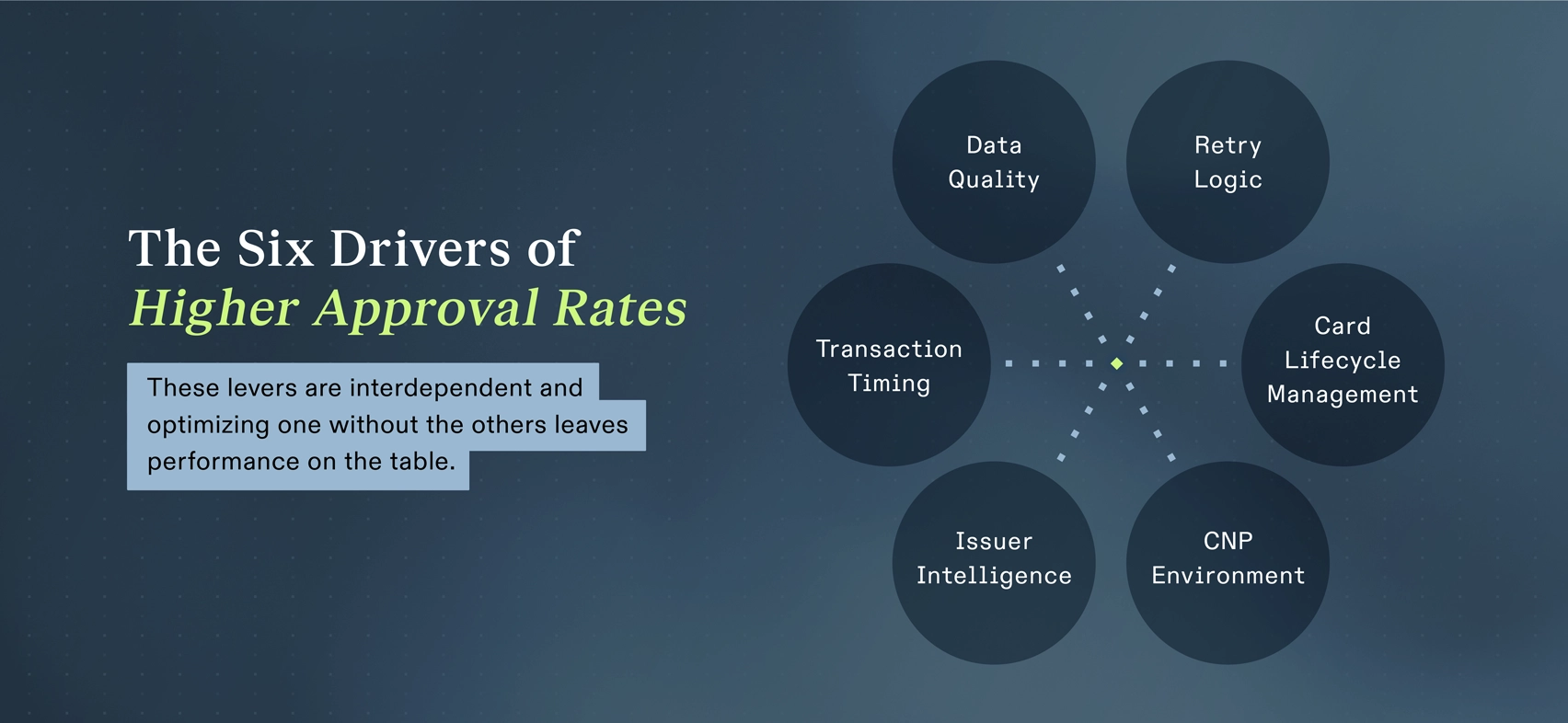

The Real Drivers of Higher Approval Rates

Approval decisions are not arbitrary. They happen in milliseconds, but they are driven by specific, identifiable signals that issuers and card networks evaluate on every transaction. Every one of those signals is something a merchant can influence. Here is where to focus.

Data Quality and Transaction Formatting

When your system submits a transaction to an issuer, you are asking them to trust you.That trust is built on the quality, completeness, and consistency of the data you send. A mismatched billing address, a name formatted differently than it appears on the card, a missing CVV, or an incorrect Merchant Category Code (MCC) — any of these can raise a flag that tips a borderline transaction toward decline.

These failures are especially hard to catch because they often happen before a transaction ever reaches the issuer for a human or algorithmic judgment call.The processor rejects it outright. It never surfaces in your standard reporting dashboards. You see a vague decline code and move on, unaware that a fixable data error was the culprit. According to Chargeback Gurus, as much as $20 billion in valid transactions are rejected every year — many of them due to exactly this kind of preventable formatting error.

Merchants who have not audited their transaction data hygiene practices are likely bleeding approval rate on payments they should be winning. This is one of the highest-ROI places to start, because the fixes are often straightforward —standardizing address formats, ensuring MCC codes are accurate and current,verifying that required authentication fields are always populated. None of this requires new infrastructure. It requires attention.

Intelligent Retry Timing and Logic

Most billing platforms come with default retry logic: a fixed schedule that retries failed payments at the same interval, using the same approach, regardless of why the payment failed in the first place. This is the payments equivalent of knocking on a door every 12 hours without ever asking why no one answered.

Not all declines are created equal. A card declined because of a temporary hold will resolve differently than one that is over its credit limit, which behaves differently from one flagged for a behavioral anomaly. Retrying at the wrong time does not just fail — it can actively hurt you. Issuers track retry velocity, and a merchant who repeatedly attempts a declined card in a short window can be flagged as suspicious. That does not only affect the immediate transaction; it damages your standing with that issuer on future payments,compounding the problem.

According to IR's guide on involuntary churn, an estimated 10 to 20% of declines are hard declines that should not be retried at all, while the rest are soft declines —temporary issues that can often be resolved with the right timing and approach.Smart retry logic, tailored to the specific decline reason, issuer behavior,and card type, can make the difference between a recovered payment and a churned customer. It requires more sophistication than most default platforms offer, but the payoff is measurable.

Card Lifecycle Management

Cards expire. Banks reissue them after fraud incidents. Card numbers change when customers upgrade or when their issuer rolls out new technology. In most cases,the cardholder does not think to notify the merchant — from their perspective,they are still a paying customer. The problem lands entirely on the merchant's side.

Without account updater services or robust tokenization in place, the next billing cycle for that customer will fail — not because they have left, not because there is a financial problem, but because the merchant is submitting a payment to a card that technically no longer exists. This is a fixable infrastructure problem, but many businesses are not fixing it. Subscription Insider research powered by FlexPay found that failed payments drive up to 48% of all churn for subscription businesses — a significant portion of which traces back to outdated card data that an account updater would have resolved automatically.

Card lifecycle management is one of those optimizations that can be set up once and run in the background, preventing a category of decline that requires zero customer interaction to solve. The barrier is not technical complexity —account updater services are widely available through most payment processors.The barrier is attention: merchants who have not prioritized this simply do not know how much it is costing them.

The Card-Not-Present (CNP) Environment

Every online and recurring payment is a Card-Not-Present transaction — meaning there is no chip to tap, no card to swipe, and no physical presence to verify. Issuers know this, and their fraud models respond accordingly. CNP transactions face significantly more scrutiny than point-of-sale payments, and in 2024, CNP fraud accounted for 71% of all card fraud losses in the U.S. — which explains why issuer fraud systems are calibrated to be aggressive in this environment.

The trouble is that this aggressiveness creates enormous collateral damage for legitimate transactions. According to J.P. Morgan, while actual fraud losses represent an estimated 7% of the total cost of fraud, false positive losses amount to 19% —nearly three times more. Issuers' machine learning models evaluate thousands of signals in milliseconds, and a transaction is more likely to be flagged if the merchant is unfamiliar, the billing descriptor is unclear or inconsistent, the charge deviates from the customer's typical pattern, or the merchant's MCC is associated with higher-risk categories.

For merchants, this means actively managing how transactions appear to issuers. A clear, recognizable billing descriptor. An accurate MCC. Submission patterns that look nothing like fraud. These are not glamorous optimizations. But they influence the risk score your transactions receive, and in aggregate, they move the needle on approval rates in ways that compound over time.

Issuer-Level Intelligence and Network Data

This is the driver that separates merchants who are genuinely optimizing approval rates from those who are hoping for better outcomes without changing their approach. Different issuers weight different factors differently. One bank may prioritize address verification data above everything else. Another may rely more heavily on the cardholder's behavioral history. The optimal way to format, route, and time a transaction for one institution is not necessarily the optimal approach for another.

The challenge is that merchants working only with merchant-side data have a fundamentally incomplete picture. The approval decision happens on the issuer's side, using signals the merchant never sees. Closing that gap requires access to issuer and network intelligence — data drawn from millions of transactions that reveals how specific issuers behave, what patterns they reward, and how to structure a transaction for the best possible outcome with that particular institution.

This is precisely why Revaly’s platform is built the way it is. By integrating exclusive issuer and network data with merchant-side transaction information, Revaly gives businesses visibility into the approval moment that merchant-only analytics cannot provide. Most merchants do not have access to this layer of intelligence, which is why it represents the largest single gap in most approval rate optimization strategies.

Transaction Timing and Submission Sequencing

When a recurring charge is submitted — the time of day, the day of the billing cycle, the proximity to other charges on the same account — all of these factors feed into how an issuer scores the transaction. Payments submitted in patterns that resemble rapid-fire fraud attempts are treated differently than those that fit the profile of a routine, expected renewal.

Pre-authorization optimization is the discipline of structuring transactions for maximum issuer confidence before they are submitted. It means treating timing, sequencing, and formatting as strategic variables rather than technical defaults. Research cited by IR notes, for example, that payments submitted during nighttime hours show measurably lower success rates. These are the kinds of details most merchants have never examined — and where material gains in approval rate are still available to those who do.

Why These Drivers Stay Hidden

Understanding the drivers of approval rates is one thing. Understanding why most merchants have not acted on them is a separate and equally important question.

The most fundamental reason is organizational. Payment success tends to live in finance or billing — a back-office function, not a cross-functional strategy. Marketing does not own it. Product does not own it. Customer experience does not own it. Nobody has built a dashboard that connects declined payments to CAC efficiency, LTV degradation, or brand health. And when no one owns the metric across the organization, the incentive to optimize it upstream simply does not exist.

There is also a visibility problem that runs deeper than org structure. The most impactful drivers of approval rates — issuer-level behavior, real-time fraud model scoring, network intelligence — are largely invisible to merchants. They sit on the other side of the transaction, inside systems the merchant has no direct access to. This creates a situation where businesses optimize what they can see while the factors that matter most remain opaque.

Then there is the false decline blind spot on the P&L. When a fraudulent charge results in a chargeback, it shows up as a line item. Someone feels it. When a legitimate customer gets declined and walks away, that revenue simply never appears. There is no entry for 'revenue we should have earned but didn't.' Research from ClearSale and Sapio found that for every $1 in credit card fraud losses, merchants lost $13 by rejecting legitimate sales due to suspicion of fraud. That ratio tells the story: the invisible loss is far larger than the visible one.

Finally, the recovery-first mindset creates institutional inertia. Dunning emails feel like action. Retry campaigns generate activity in dashboards. The energy going into those efforts is real, and they do recover some revenue. But they also obscure how much prevention could have saved in the first place — and they do nothing to address the upstream conditions that caused the failure.

What a Prevention-First Approach Actually Looks Like

The shift being described here is a concrete change in how businesses think about,measure, and invest in their payment infrastructure. Most companies sit at what might be called Stage 1 of payment maturity: reactive recovery, where the question is 'how do we fix this after it fails?' Some have advanced to Stage 2: smarter dunning, better retry logic, more deliberate recovery campaigns. Butthe companies that are genuinely leading on approval rates have made a more fundamental shift.

At Stage 3, the question is entirely different: 'How do we engineer success before a payment is ever submitted?' That reframe moves optimization upstream, into pre-authorization strategy. It connects payment performance to customer retention, CAC efficiency, and revenue predictability. It turns payments from a cost center into a growth lever.

The business case is straightforward. A business processing $100 million in annual transaction volume captures an additional $1 million in revenue for every single percentage point of improvement in its approval rate. Those gains come from existing demand — customers who already want to pay — without requiring a dollar of additional marketing spend. For subscription and recurring billing businesses, the effect is even more pronounced, because each prevented decline is also a churn event avoided, extending customer lifetime value and improving the return on every dollar spent on acquisition.

Practically, a prevention-first approach involves a few key shifts working in concert:

- Treating data quality as a payment performance issue, not just a compliance one — auditing transaction formatting, MCC accuracy, and billing descriptors on a regular basis.

- Replacing default retry logic with intelligent, decline-reason-aware strategies tailored to specific issuer behaviors and card types.

- Implementing account updater services or tokenization to manage card lifecycle changes proactively rather than reacting after a billing cycle fails.

- Gaining access to issuer and network intelligence that provides visibility into the factors driving approval decisions on the other side of the transaction.

- Measuring payment success at the revenue capture level — not just authorization rate — so the full impact of optimization is visible to the organization.

This is the kind of unified, intelligence-driven approach that platforms like Revaly are built to enable. Rather than fragmenting these capabilities across multiple vendors, the goal is a single system that optimizes the full transaction lifecycle — before, during, and after authorization — and gets smarter with every payment it processes.

Approval Rates Are a Strategic Lever, Not a Backend Metric

Here is the core idea worth holding onto: approval rates are not something that happen to your business. They are something your business shapes — through the quality of your transaction data, the intelligence of your retry logic, the care you take with the CNP environment, and the upstream decisions you make before a paymentis ever submitted.

Most merchants are not operating with that understanding. They are reacting to declines instead of engineering approvals. They are measuring authorization rates instead of revenue capture. They are treating payments as infrastructure instead of strategy. And the result is a persistent, invisible revenue leak —not because customers do not want to pay, but because the system was never designed to make sure legitimate payments succeed.

The merchants who close this gap will find that one of the most powerful growth levers in their business was sitting inside their payment stack the entire time, waiting for someone to pay attention to it.

Every legitimate transaction should be approved by design, not by chance. To go deeper on what payment performance management looks like in practice — and how Revaly helps businesses engineer above-market approval rates — explore the full eBook: Approvals by Design: Why Payment Performance Management Is the Next Growth Engine.