Key facts

- Most subscription payment declines aren’t due to fraud or insufficient funds.

- Issuers often decline legitimate transactions because they lack context or trust in the data submitted.

- In many subscription businesses,up to 70% of churn is involuntary, driven by failed payments.

- Small improvements in approval rates (2–3%) can unlock millions in revenue and create real competitive advantage.

- The solution isn’t “retry more.”It’s about improving the quality, consistency, and credibility of the data reaching the issuer before a decline occurs.

Subscription businesses don’t have a customer problem — they have a signal problem.

In our recent webinar, Good Customers, Bad Outcomes, we unpacked a pattern we see repeatedly across recurring billing portfolios: legitimate customers with valid cards are being declined not because they can’t pay, but because the issuing bank doesn’t have enough confidence to approve the transaction.

This isn’t about fraud spikes or customer intent. It’s about how transactions are evaluated at the authorization layer — and where critical context gets lost.

The Cost of Payment Declines in Subscription Businesses

Most merchants treat approval rates as a surface-level metric. A 95% approval rate feels strong, but in a recurring revenue model,even small gaps translate into significant financial consequences.

Consider a $50 million subscription business operating at that rate. A 5% decline rate represents $2.5 million in lost revenue annually, before accounting for lifetime value. When a renewal fails andthe customer churns, the impact is deeper than a single billing cycle — you also lose future expansion revenue, the acquisition cost already invested, and downstream retention opportunities.

In fact, research shows up to 70% of total churn in subscription portfolios is involuntary — customers didn’t choose to leave;their payment simply failed. What looks like a technical issue is actually a revenue leak.

Why Legitimate Payments Still Get Declined

When a payment reaches the issuing bank, the decision isn’t simply “Is this fraud?” Issuers are processing hundreds of data points in milliseconds, and if anything about that signal appears uncertain or inconsistent, the safest choice for the bank is to say “no.”

Issuers evaluate questions like:

- Does this transaction match historical behavior?

- Is the data complete and formatted correctly?

- Does this merchant carry elevated risk indicators?

If banks can’t confidently answer these questions, they may decline — even if the customer has sufficient funds and a valid card.

This dynamic is especially common in recurring billing environments, where renewals are processed without the customer present, often with limited contextual data attached.

The result is what we call good customers, bad outcomes.

If you want to go deeper into why approval rates deserve strategic focus, check out Revaly’s guide, The Approval Rate Playbook: How to Prevent Failures From Happening, which walks through why focusing on preventing declines is more powerful than recovering them.

The Three Recurring Blind Spots in Subscription Payments

Over years of portfolio analysis, we’ve identified three structural friction points that consistently contribute to avoidable declines.

1. Stale or Reissued Credentials

Expired cards are obvious, but reissued cards — due to fraud, upgrades, or bank changes — are less visible and more damaging. When credentials aren’t captured and refreshed, renewals fail.

In many portfolios, up to half of hard declines originate from stale credentials. Tools like Card Account Updater help, but they aren’t perfect and should not be treated as set-and-forget solutions.

2. Inconsistent Recurring Indicators

Transaction-level signals — like recurring flags,merchant-initiated indicators, and proper Merchant Category Codes (MCC) — help issuers interpret intent. When these signals are inconsistent or rely on defaults without auditing, issuers may evaluate transactions as higher risk than intended.

Many teams don’t fully understand how descriptors or MCCs influence issuer interpretation, yet issuers weigh them heavily.

3. Lost Context

Issuers evaluate each transaction independently unless context is explicitly conveyed. If renewals aren’t tagged in a way that communicates historical relationship or intent, that history doesn’t factorinto the decision.

In recurring billing scenarios, lost context is one of the most common drivers of soft declines.

For a more comprehensive look at how payment success ties to customer retention across billing events — and not just declines — see Revaly’s Optimizing Payment Success Across all Subscription Billing Events guide.

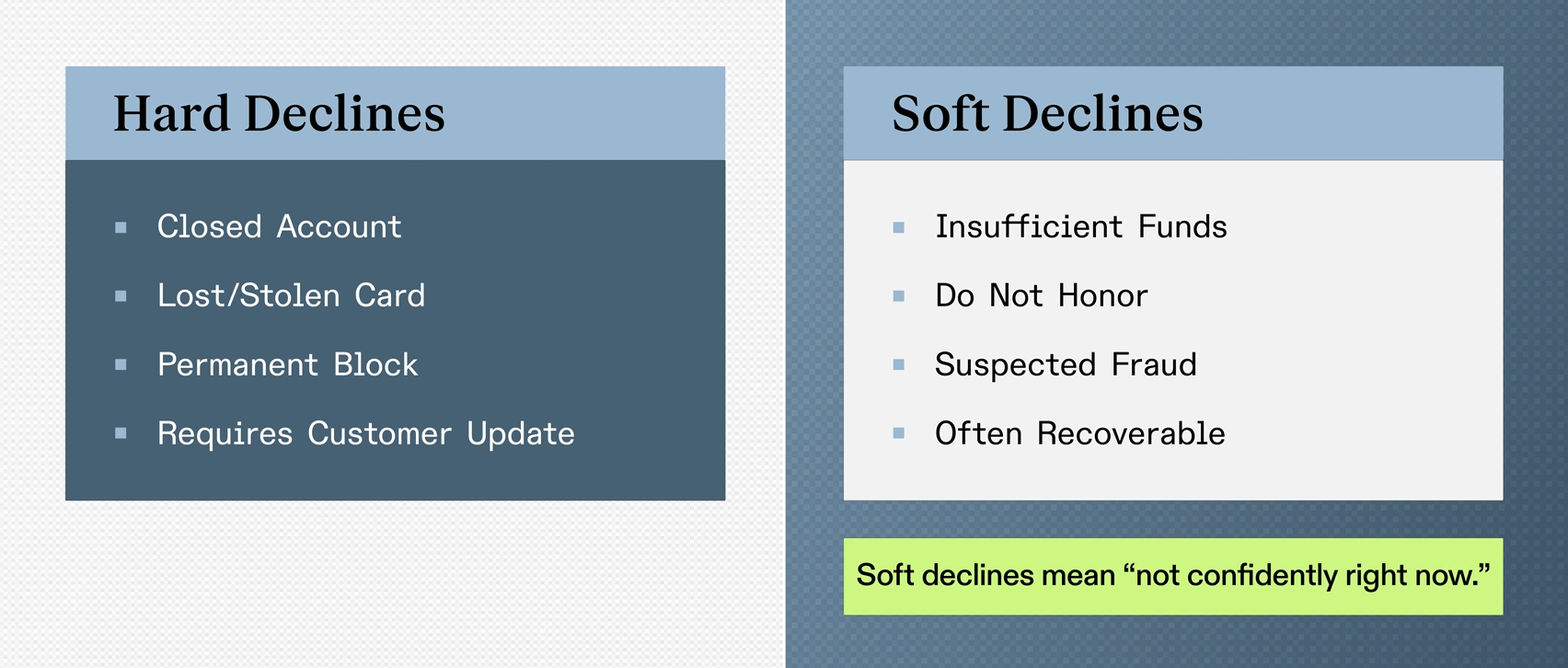

Soft Declines vs. Hard Declines

Not all declines are created equal.

Hard declines — like closed accounts or permanently blocked cards — require customer intervention. Soft declines — such as “Insufficient Funds,” “Do Not Honor,” or “Suspected Fraud/Pick Up Card” — are often recoverable.

Three of the most common response codes fall into this soft category. They don’t mean “never”; they mean “not confidently right now.” And yet many merchants treat all declines the same: retry aggressively or send generic dunning — approaches that often make outcomes worse.

Why “Retry More” Isn’t a Strategy

Visa has expanded the allowable retry window for soft declines — technically permitting up to 20 retries within 30 days. But just because you can retry doesn’t mean you should.

Retrying too aggressively can:

- Increase decline ratios

- Damage merchant reputation

- Lower first-attempt approval rates over time

Issuers track merchant behavior, and elevated failed paymentrates influence how future transactions are evaluated. In simple terms: failed payments can lead to more failed payments.

At the same time, retrying too conservatively leaves revenue on the table.

Strategic retries must consider:

- Response code

- Timing patterns

- Customer payment behavior

- Issuer-specific performance

- Portfolio-level trends across your entire customer base

There is no universal retry cadence that works for every business.

For a deeper metric-focused perspective on measuring payment performance beyond simple authorization rates — including how to capture true payment success — see Beyond Authorization Rates: A Smarter Way to Measure Payment Performance.

The Communication Problem at the Authorization Layer

At its heart, this isn’t fundamentally a processing issue —it’s a communication issue.

Every transaction sends a structured ISO message containing dozens of fields — metadata, indicators, identifiers, and contextual flags.Issuers use this packet of information to decide whether to trust the transaction.

If the message is incomplete, inconsistent, or poorly formatted, the bank defaults to caution.

Improving approval rates requires improving the clarity,completeness, and credibility of what reaches the issuer. That means auditing:

- Gateway formatting

- Field population

- MCC assignments

- Descriptor clarity

- Recurring indicators

- Credential freshness

- Retry logic

Most teams rely on abstractions built into gateways and billing systems. While convenient, these abstractions don’t guarantee optimization.

What’s Changing in 2026

The authorization environment is changing rapidly.

Fraud data is becoming noisier, and issuers struggle to differentiate between true fraud and first-party disputes. When fraud models are trained on incomplete data, they become more conservative — increasing false declines.

Meanwhile, authentication standards are evolving across North America and Europe, and regulatory changes are tightening how identity and consent signals are transmitted. Outdated authentication flows will increasingly show up as degraded approval performance.

At the same time, we’re seeing merchants create measurable 2–3% approval gains through proactive optimization. Those gains compound:higher approval rates mean lower effective acquisition costs, faster payback periods, and stronger lifetime value.

The result? Approval rate optimization is no longer operational hygiene — it’s competitive leverage.

For a strategic perspective on how payment performance evolves into a revenue engine for growth, check out Approvals By Design: Why Payment Performance Management is the Next Growth Engine.

Where to Start

Before changing retry logic or deploying new tools, begin with an honest evaluation of your data.

Measure:

- First-attempt approval rate (notjust overall approvals)

- Involuntary vs. voluntary churn

- Decline code distribution

- Recovery rate by response code

- Approval trends after policy or gateway changes

Most companies stop after looking at approved vs. declined totals. But what gets measured gets managed — and what isn’t measured compounds into a significant problem.

The Bottom Line

Most subscription payment declines aren’t customer failures— they’re signal failures. The issuer isn’t rejecting your customer; it’s rejecting the information it received. When the data lacks clarity,consistency, or context, the bank’s safest decision is to decline.

Soft declines represent revenue that could have been approved, but only when approached with strategy and precision. Blindretries and generic dunning sequences won’t fix structural issues. Optimizing approval rates requires understanding how issuers evaluate risk, how data is formatted and transmitted, and how merchant behavior influences future decisions.

The revenue you’re chasing isn’t outside your business —it’s already inside your portfolio. The real question is whether your payment data gives issuers enough confidence to release it.

And as optimization capabilities advance, the performance gap between merchants who actively manage approval rates and those who don’t continues to widen. The only question left is: which side of that gap are you on?

Want to start preventing payment failures? Talk to our team and learn how Revaly helps merchants engineer approvals instead of chasing losses.