Involuntary churn is a revenue problem that most subscription businesses have simply accepted as inevitable. A card declines, a retry fires at the wrong moment, and a subscriber disappears. The business records it as a loss, moves on, and assumes the system is working as intended.

That assumption is expensive. In a recent conversation hosted by Revaly, two Revaly clients — Nick Reshamwalla, V P of Engineering and Data at Dollar Shave Club, and Yanick Gianesin, Global Payments and Risk Manager at Immunotec — sat down to share what involuntary actually cost them, and what changed when they stopped accepting it.

The full conversation covered a lot of ground. Here's what stood out.

Retry logic is less logical than most teams think

The gap between "configured"and "optimized" is wider than it looks, and most businesses don't realize it until they measure it.

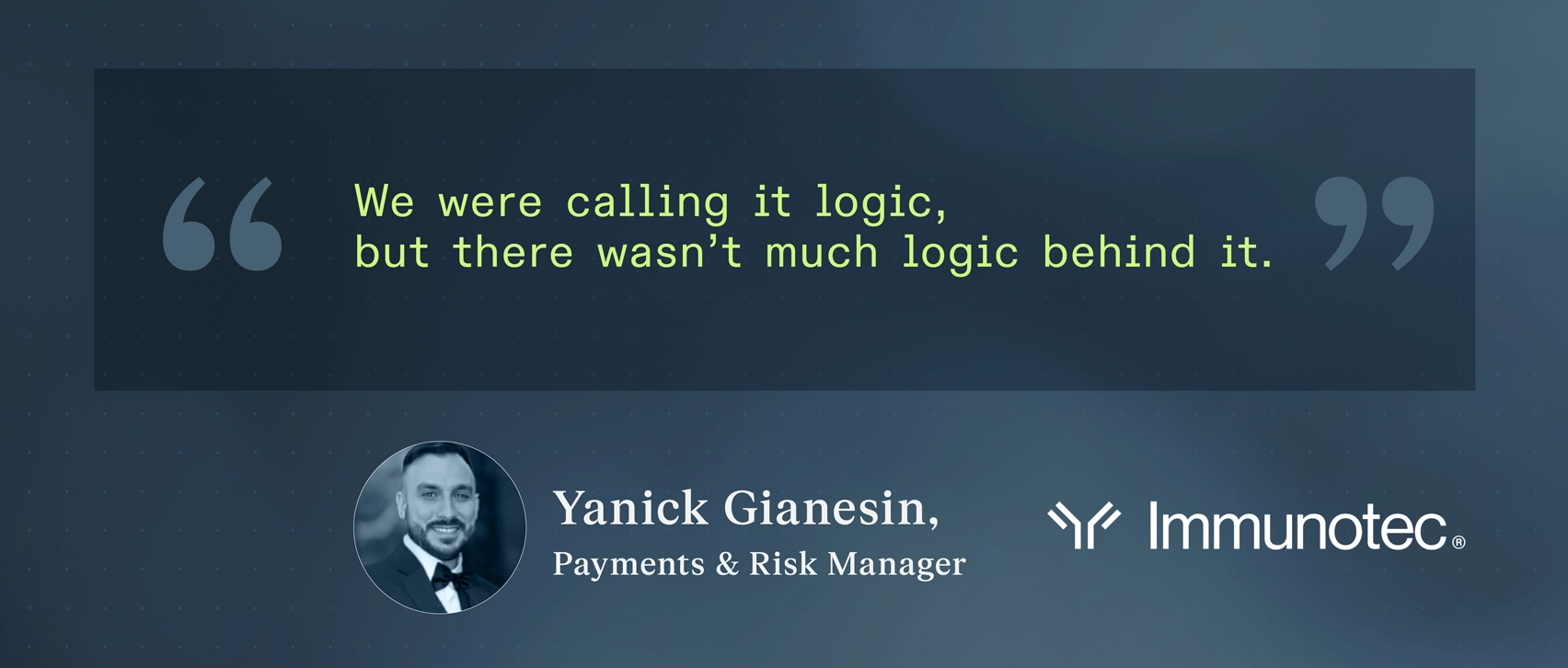

At Immunotec, a subscription network operating across North America, Latin America, and Europe, the retry setup had been manually tuned over years: intervals adjusted, attempt counts changed,timing tweaked. Recovery rates were in the low single digits. Yanick's assessment was unsparing: "I'll be honest with you — we were calling itlogic, but there wasn't much logic behind it."

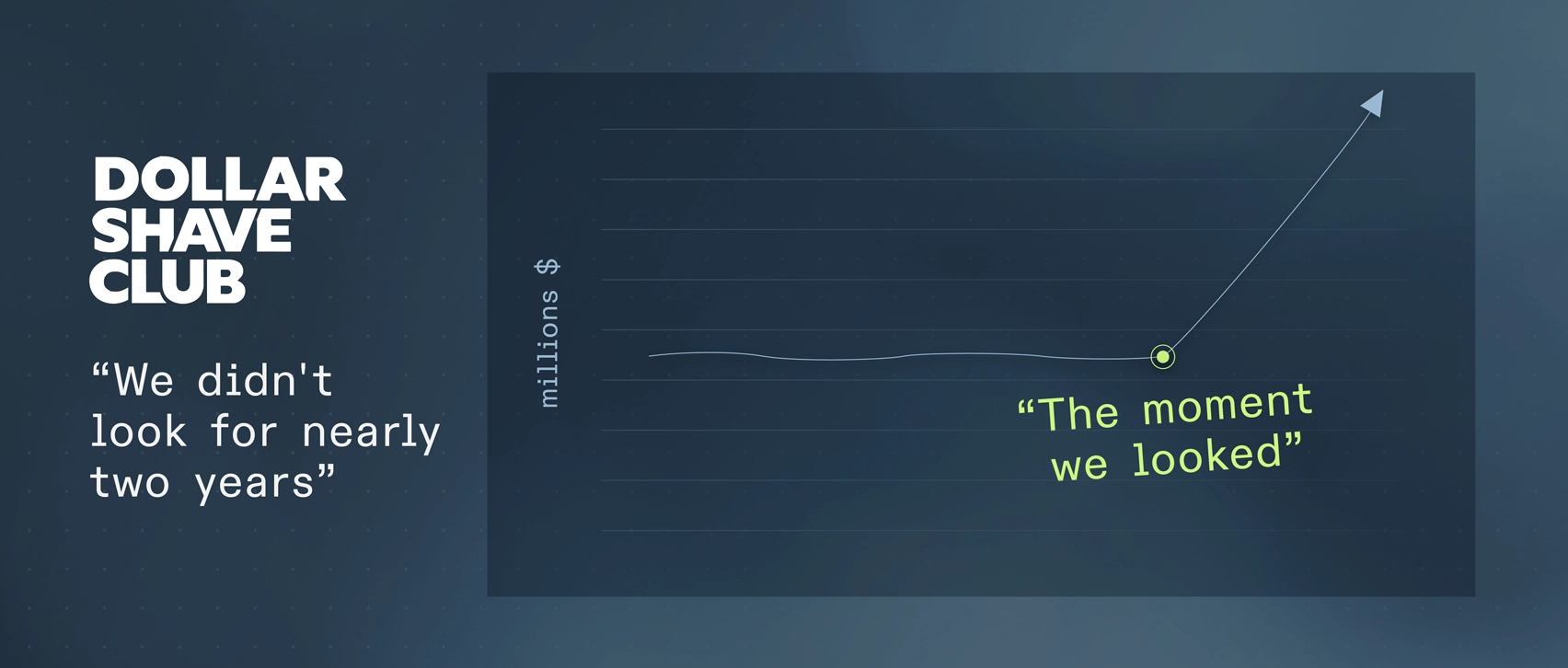

Dollar Shave Club ran a rules-based,static approach and had tested different cadences without meaningful results.Nick's team had gone nearly two years without seriously revisiting the setup — not because they had decided it was working, but because nothing was visibly broken. When Revaly asked webinar attendees when they'd last reviewed their retry logic, most answered: "a while ago." And that makes sense because in many subscription businesses, the payments function sits with one person managing a hundred priorities, and configured systems become invisible until they become a crisis.

The starting point for both companies wasn't a failed system; it was an unexamined one. That distinction matters because the fix isn't just technical. It starts with deciding to look.

More retries isn't the answer — and can make things worse

Once teams do look, the instinct is toretry more aggressively. It feels like the right thing to do, but it isn’t.

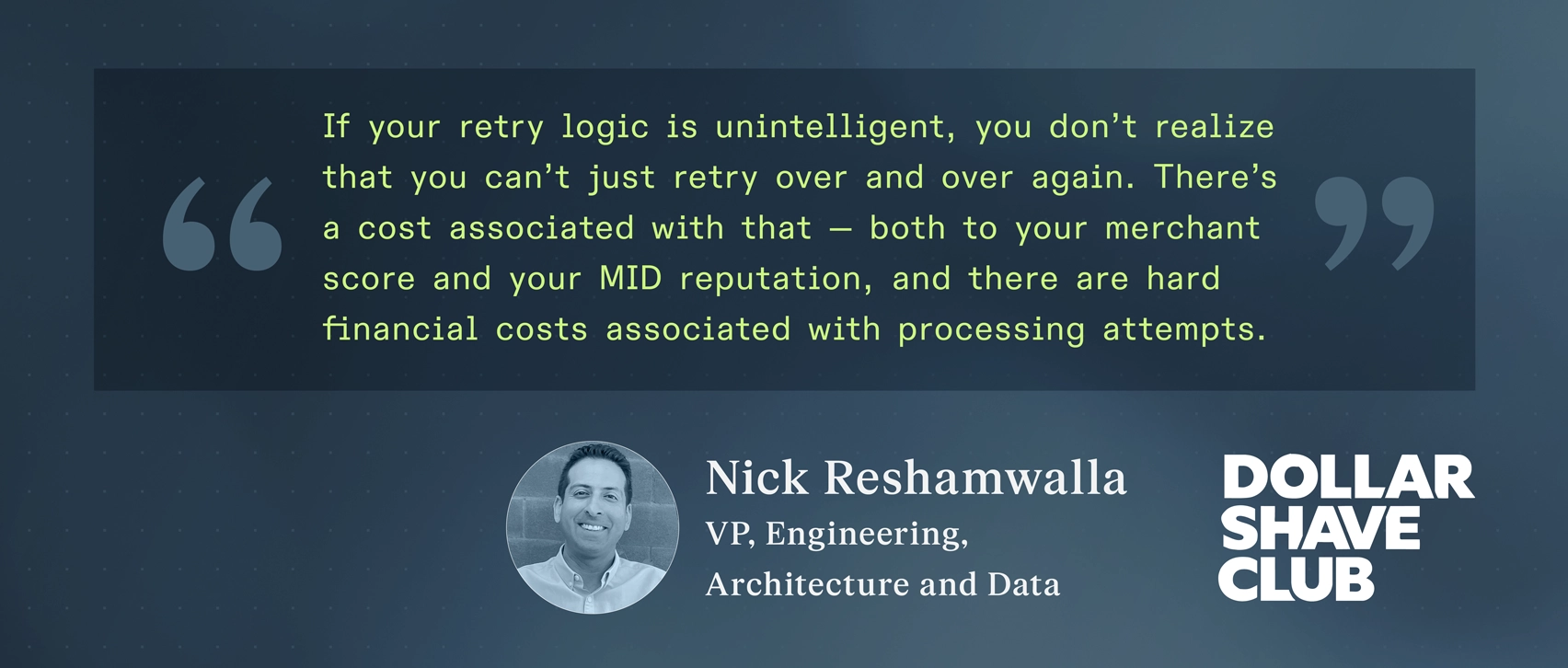

Retrying without intelligence —applying the same rules regardless of decline reason, payment method, or customer history — produces two distinct costs. The direct cost is processing fees against attempts with near-zero probability of converting. The less visible cost is what it does to your merchant standing: Visa and Mastercard track retry behavior, and elevated failure rates affect how future transactions are evaluated. An aggressive retry strategy doesn't just fail to recover revenue. It can actively increase the likelihood of future declines,compounding the problem it was meant to solve.

As Nick put it: "If your retry logic is unintelligent, you don't realize that you can't just retry over and over again. There's a cost associated with that — both to your merchant score and your MID reputation, and there are hard financial costs associated with processing attempts."

Revaly's platform is built specifically to give subscription teams that visibility, replacing static retry rules with intelligent, signal-driven decisioning. The real discipline is equilibrium: knowing which signals predict recovery, when to stop, and what an attempt costs relative to its expected yield. But equilibrium looks different depending on where in the subscription lifecycle a payment fails.

First rebill failures are a customer acquisition problem, not just a payments problem

Not all failed payments carry equal weight. A renewal failure is painful, but the customer has been generating income from months, a strong relationship exists, and recovery is possible. A first rebill failure is a different kind of loss entirely. The acquisition cost has already been spent, and the customer is almost certainly gone before they ever convert into a long term subscriber.

At Dollar Shave Club, which frequently acquires subscribers through low-cost entry offers, a failed first rebill means the economics of the acquisition never close. Nick's team has made progress identifying which payment method signals predict first rebill failure, allowing them to anticipate the problem rather than react to it, but his larger issue was about framing. Most businesses treat this as a payments issue, but it’s also a CAC problem, and recognizing that changes how much you're willing to invest infixing it. For Nick and Yanick, that’s what the numbers ultimately came down to.

What the numbers look like on the other side

After partnering with Revaly, both companies moved from single-digit to double-digit recovery rates. Immunotec went from 3–5% up to 30% — and sometimes nearly 50% — depending on the market. For Dollar Shave Club, the shift translated to millions of dollars in annual recovered revenue.

The second-order effects were equally notable. Yanick found that fewer retries against accounts that were never going to convert reduced noise in the system, improved overall authorization rates,and left a healthier merchant profile. Getting smarter about when not to retry turned out to matter as much as getting smarter about when to.

For Nick, the more unexpected benefit was data visibility. His team could suddenly ask questions they hadn't been able to before, including:

- What does lifetime value look like for a customer who came in on a specific payment method?

- How should pricing account for what they now know about payment behavior and risk?

What had started as a recovery problem had become a source of strategic clarity, one that's available to any subscription business willing to give payments the attention they deserve.

The question isn't whether to fix it. It's how long you can afford not to.

Nick and Yanick both feel it’s imperative to look at your retry logic and look at it now. Not because something is visibly broken, but because the gap between where most businesses are and where they could be has a real dollar value attached to it — one tha tcompounds as it goes unexamined.

Nick had done the math on his own two-year gap. He wouldn't share the number, but his description of it was stark: "a big number." His only regret was not looking sooner.

If you're not sure the gap exists in your business, run a test. A/B testing retry cadences has low cost and high information value. Businesses that have closed the gap — and turned payments data into a strategic asset in the process — didn't get there by waiting for something to break. They got there by deciding that tolerating the problem was more expensive than solving it. Revaly is how subscription businesses make that decision actionable, replacing guesswork with payment performance intelligence that tells you exactly where the gap is and what it's costing you.

Watch the full recording of Peers in Payments: Subscription Edition, or talk to our team to see what payment performance could look like for your business.