Issuing banks rely on well-defined (and constantly evolving) models to determine whether a transaction is safe, legitimate, and correctly formatted. Because issuers prioritize cardholder protection over merchant revenue, even minor inconsistencies can escalate into a payment declined by card issuer event. When merchants understand how these models work—and where they can influence them—they dramatically improve approval rates.

Let’s dive into what happens behind the scenes and the steps merchants can take towards reducing card issuer declines using Revaly’s prevention-first approach.

The Type of Transaction with the Most Issuer Declines

Card-Not-Present (CNP) purchases make ecommerce and subscription businesses possible, but they also create the highest share of issuer declines. In a physical, in-person payment, the cardholder hands over the card and identity verification is more direct. But with CNP, all the issuer or payment network sees is metadata (card number, billing address, IP, device/browser info, token, etc.). That limited context makes it much harder to distinguish between genuine customers and fraud attempts — so issuers err on the side of caution.

As a result, false declines (i.e. valid CNP payments that get rejected) are a major pain point in ecommerce and subscription billing. Some data points that illustrate why:

- A survey by the Merchant Risk Council found that the average online store declines about 2.6% of all orders because of suspected fraud — even when the orders are legitimate.

- For larger or higher-value purchases, false declines are even more common. According to one source, orders over $100 are more likely to be wrongly declined than smaller ones.

- Research suggests that up to 15% of card-not-present (CNP) transactions are falsely flagged as fraudulent, causing annual revenue losses of $118 billion.

A Deep Dive into Why Valid Payments Get Declined

Issuer decline logic has become more conservative in recent years, especially in online and subscription commerce. Key factors driving issuer declines include:

Fraud & Risk Modeling Sensitivity

Issuers analyze multiple risk signals to decide whether a transaction is safe. These include:

- IP address reputation – Is the IP linked to suspicious activity or high-risk regions?

- Device fingerprint consistency – Does the device match previous patterns for this cardholder?

- Sudden shifts in spending patterns – Unusual purchase amounts or frequency can trigger alerts.

- Velocity and location mismatches – Multiple transactions in a short time or from different locations may look fraudulent.

- VPN or proxy usage – These can hide the true location, which issuers often treat as a red flag.

Why this matters

Fraud attempts are significantly higher in CNP commerce because the card isn’t physically present. Issuers have limited context and rely heavily on these signals, so even legitimate transactions can be declined if they appear risky.

Weak or Incomplete Metadata

Metadata in payments refers to all the supporting information sent along with a transaction, such as billing address, card verification details, authentication indicators, and currency codes.

If this metadata is missing, inconsistent, or incorrect, the issuer may reject the transaction before even running fraud risk scoring because the request looks incomplete or non-compliant.

Examples of problematic metadata:

- Billing address mismatches – The address provided doesn’t match what the issuer has on file.

- Outdated tokens – Tokens used for stored cards are expired or not refreshed.

- Missing 3DS or SCA indicators – No proof of authentication or compliance signals.

- Incorrect AVS or CVV fields – Wrong or missing security codes.

- Currency and country code errors – Poorly formatted or mismatched codes.

Why this matters

Metadata hygiene is one of the easiest issues to fix, yet it causes a large share of declines. Clean, complete, and standardized metadata improves issuer confidence and approval rates.

Card Lifecycle & Token Issues

Card lifecycle problems occur when a card’s status changes but the merchant’s system isn’t updated:

- Card lifecycle problems occur when a card’s status changes but the merchant’s system isn’t updated:

- Expired cards – The card has passed its validity date.

- Reissued or replaced cards – The bank sends a new card (e.g., after loss or fraud), but the old details are still stored.

- Expired cards – The card has passed its validity date.

- Token issues relate to digital security tokens used instead of actual card numbers:

- Unrefreshed tokens – Tokens linked to old card details aren’t updated.

- PAN (Primary Account Number) token mismatches – The token doesn’t match the card number expected by the issuer.

- Network tokenization inconsistencies – Errors in how tokens are generated or recognized across payment networks.

- Unrefreshed tokens – Tokens linked to old card details aren’t updated.

Why it matters

Issuers see mismatched or outdated data as risky or invalid, so they decline the transaction. This is especially harmful in subscription billing because:

- Customers usually don’t know their payment failed.

- Merchants lose revenue and risk customer churn.

Suboptimal Routing Decisions

This refers to how the path a payment takes through processors and networks can significantly affect whether it gets approved or declined.

Why it matters

When a customer makes a payment, the transaction is routed through various processors before reaching the card issuer for approval. Processor performance fluctuates, however, meaning some routes have higher success rates than others.

Factors influencing routing success include:

- Issuer/processor relationships – Some processors have stronger ties with certain banks, leading to better approval rates.

- Region – Cross-border transactions may face more scrutiny.

- Card type – Different card brands (Visa, Mastercard, etc.) may perform better on certain routes.

- Network traffic patterns – High traffic or congestion can impact performance.

If merchants use static routing (fixed paths for all transactions), they risk sending payments through routes with higher decline rates.

- Dynamic routing, which adjusts paths based on real-time performance, can reduce declines and improve approval rates.

Authentication & Compliance Requirements

Issuers prioritize security and regulatory compliance, such as:

- Strong Customer Authentication (SCA) fields – These show that the transaction meets regulatory standards (like PSD2 in Europe), using two or more factors (e.g., password, device, biometric).

- 3DS2 authentication outcomes – Successful results from the 3-D Secure 2 protocol (which verifies the cardholder’s identity during online payments) boosts approval chances.

- Network-required metadata – Specific data fields mandated by card networks (e.g., Visa, Mastercard) to confirm compliance and reduce fraud risk.

Why it matters

If these indicators are incomplete or missing, the issuer cannot confirm the transaction’s legitimacy or compliance, so the payment is declined—even if it’s valid.

The Real Cost of False Declines

Because false declines are relatively invisible (customers just see “declined”), they carry enormous costs:

- Lost sales and revenue — Every declined but valid transaction is a lost sale. For high-volume merchants, even a modest false-decline rate can translate into substantial monthly or annual revenue leakage.

- Customer frustration and churn — For many consumers, a single declined payment feels like a personal rejection; when a legitimate CNP payment fails, a significant portion of shoppers never return. For example, a report shows that a large share of customers abandoned a brand altogether after a false decline.

- Reduced lifetime value (LTV) — Especially in subscription or membership models, a false decline can interrupt renewal cycles or ongoing billing — causing involuntary churn and reducing customer LTV.

- Increased support load and operational cost — Declines often generate customer support inquiries, complaints, and retries. Merchants may spend time and resources chasing down root causes — often without success if data is fragmented.

- Brand and trust damage — If customers repeatedly experience unexplained declines, their confidence in the merchant declines — potentially pushing them to competitors and damaging long-term brand reputation.

How Revaly’s Payment Performance Management Platform Increases Approvals

False declines are now responsible for more lost revenue than actual fraud in many ecommerce sectors and merchants rarely know how to diagnose them. But improving approval rates doesn’t require guessing. It requires clarity, hygiene, and the right intelligence tools.

Unfortunately, most teams lack the ability to execute these effectively in a complex, multi-system payment stack.

That’s where Revaly changes the game.

Revaly is built specifically to reduce the types of issues that cause issuer declines in ecommerce and subscription billing with a prevention-first approach to improve payment approval rates.

Given the complexity and hidden nature of decline causes, Revaly’s Payment Performance Management platform becomes especially powerful. Here’s how:

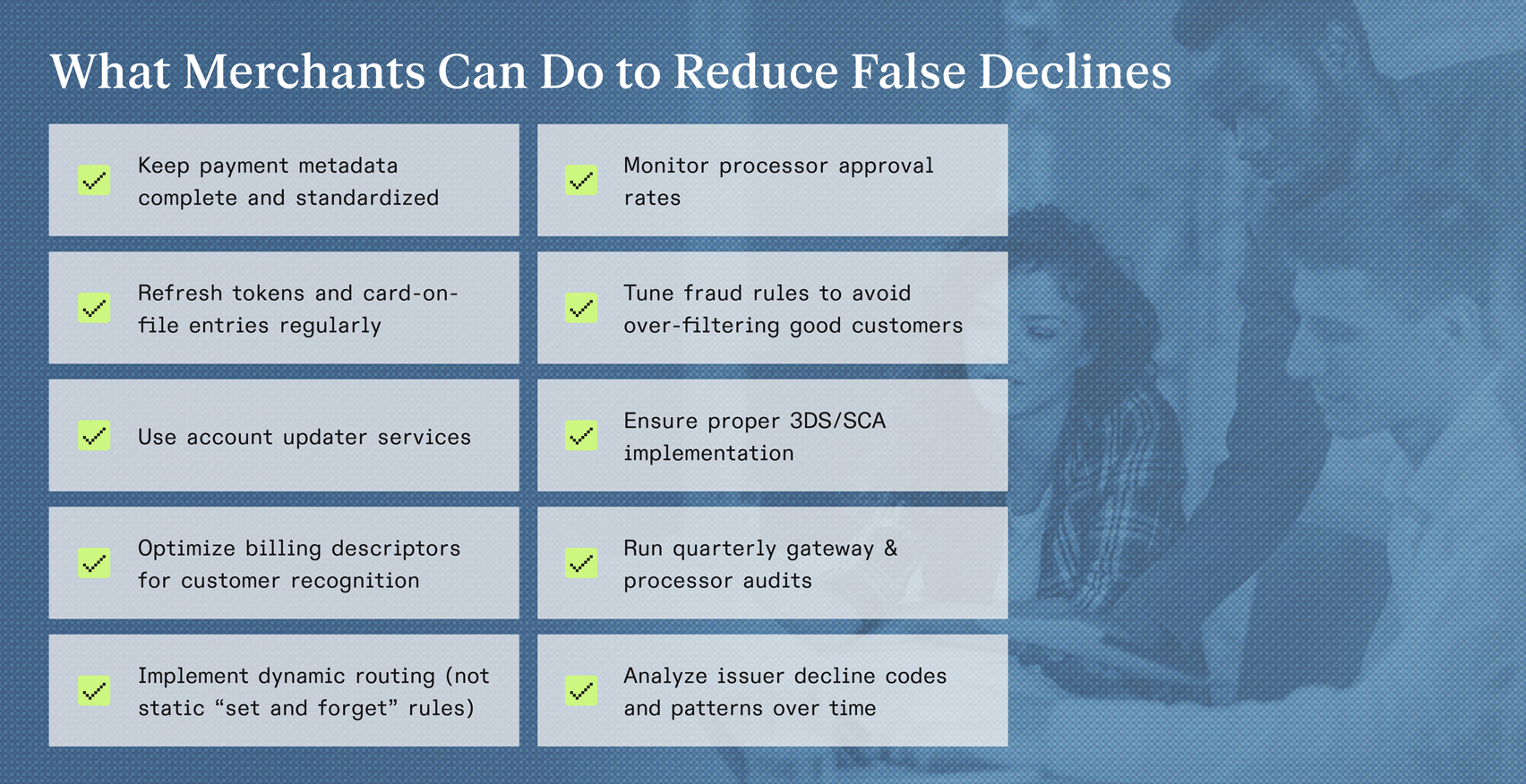

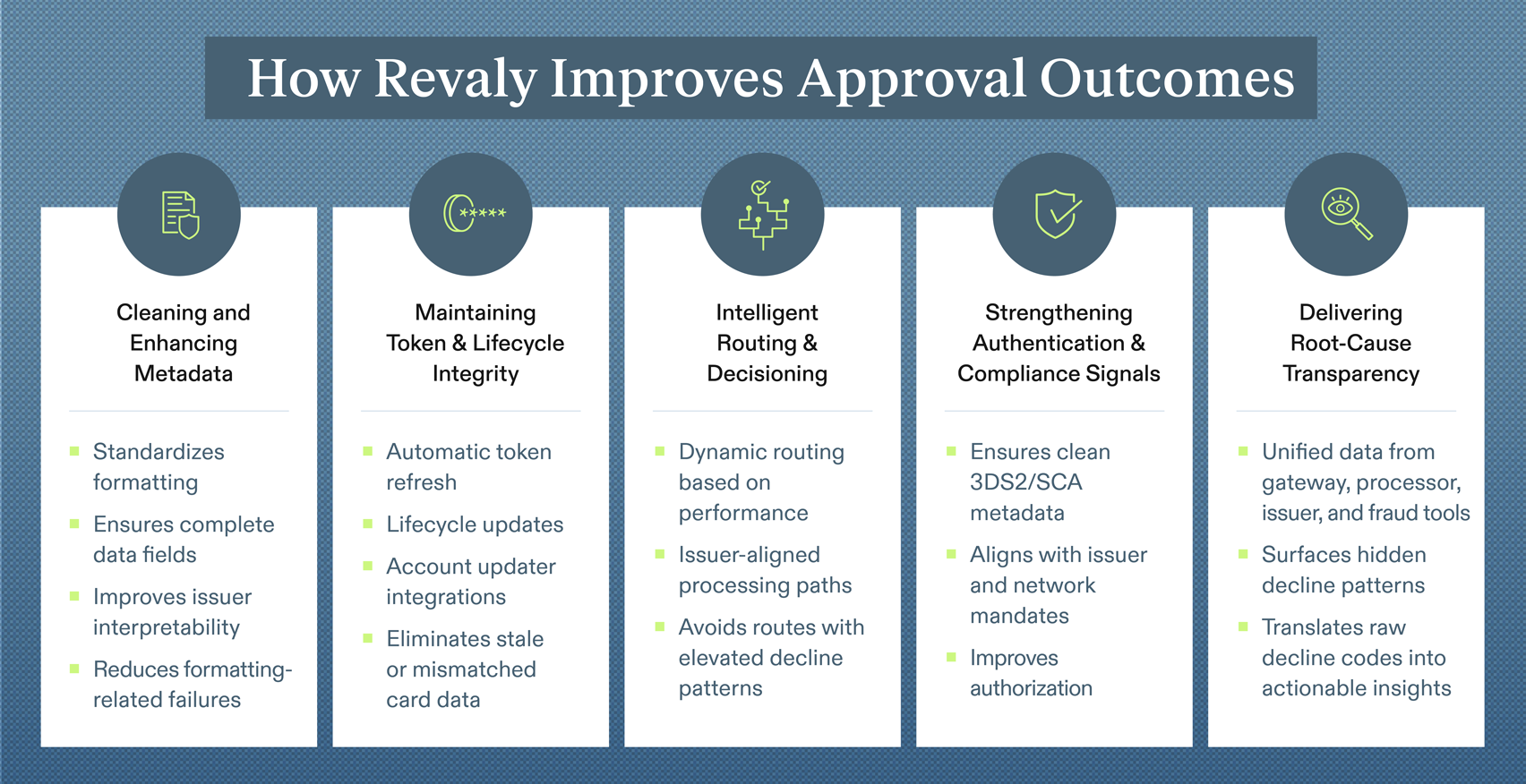

- Unified intelligence powering better decisions - Revaly unifies merchant-side payment data with issuer and network intelligence inside our platform to understand why transactions succeed or fail. By normalizing signals across gateways, processors, fraud tools, tokenization layers, and response patterns, Revaly identifies the patterns and root causes behind preventable failures (e.g., formatting gaps, metadata issues, timing mismatches, stale tokens). This intelligence drives the treatments and optimizations that improve approval performance, without requiring merchants to manage data or interpret complex decline signals themselves.

- Token & metadata hygiene automation - Revaly helps ensure that card-on-file data, network tokens, billing metadata (address, currency, device fingerprint) and other request parameters are correct and up to date, reducing declines caused by technical mismatches rather than genuine risk.

- Dynamic routing & retry logic optimized for CNP flows - For online transactions, where network performance, processor health, card type, issuing region and fraud models vary widely, Revaly’s routing logic can automatically choose the best path or reattempt failed authorizations, boosting likelihood of approval even when the first attempt fails.

- Root-cause analytics & reporting - By centralizing decline codes, customer behavior, and transaction metadata, Revaly helps merchants move beyond guesswork. They can then identify systemic issues (e.g. a pattern of tokenization-related declines, or a certain processor underperforming during specific hours) and proactively fix them, rather than reacting to symptoms one decline at a time.

Reducing Card Issuer Declines Requires Visibility — Not Guesswork

In the world of ecommerce and subscription billing, some issuer declines are inevitable, but the majority of them are preventable. Most failures stem from incomplete metadata, outdated tokens, suboptimal routing, misaligned authentication signals, or overly sensitive fraud logic. Merchants who treat approvals as a performance discipline—rather than a passive outcome—recover significant revenue and deliver a smoother customer experience.

Revaly gives merchants this control.

Revaly prevents payment declines by continuously optimizing how transactions are formatted, routed, and presented to issuing banks using real-time intelligence and direct issuer relationships to improve approval rates and keep valid customers on board for months to come.

If you’re ready to reclaim lost revenue and reduce issuer declines, reach out to Revaly team and have a conversation.