You check your churn dashboard on Monday morning like you always do and notice the numbers have risen again. No surprises there, unfortunately. But here's what most teams miss in that moment: not all churn is the same. A significant share of it is involuntary churn — customers who didn't choose to leave. Their payment failed, the subscription lapsed, and the relationship ended without either side wanting that outcome. What happens next is almost always the same: the product team evaluates features, customer success gets a higher satisfaction mandate, and someone starts talking about win-back campaigns. And while it feels like you're doing all the right things, in reality you're probably focused on the wrong problem.

What? Churn is churn, right?

Wrong.

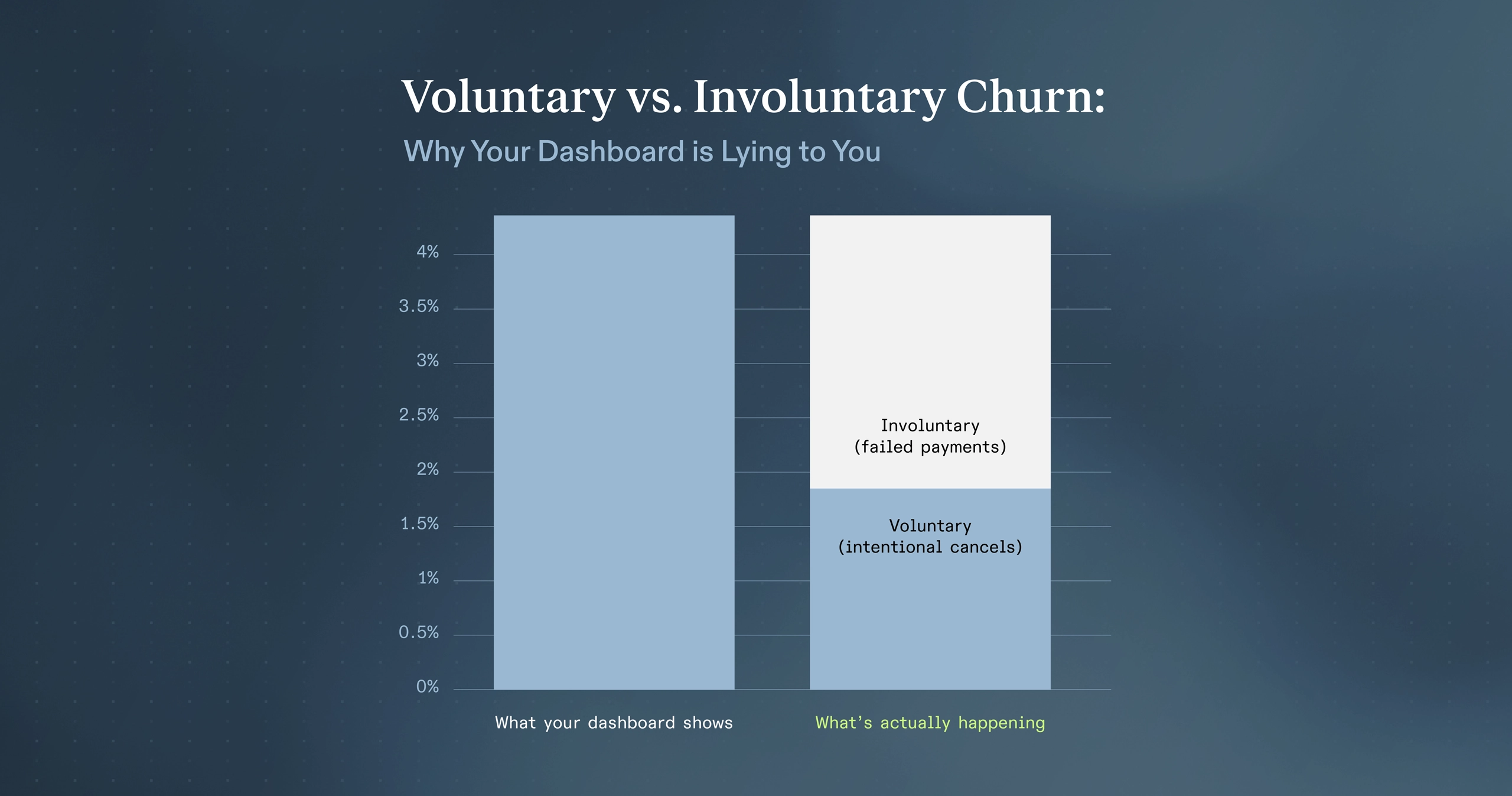

The number on that dashboard — the one you're treating as the signal to take action— is almost certainly a blend of churn: voluntary and involuntary. It's mixing two fundamentally different events: customers who chose to leave, and customers who were pushed out by a payment failure they never saw coming and may not even know happened. Those two situations require completely different responses, but when you can't tell them apart, you're making critical business decisions based on faulty information.

Voluntary vs. Involuntary Churn: Know the Difference

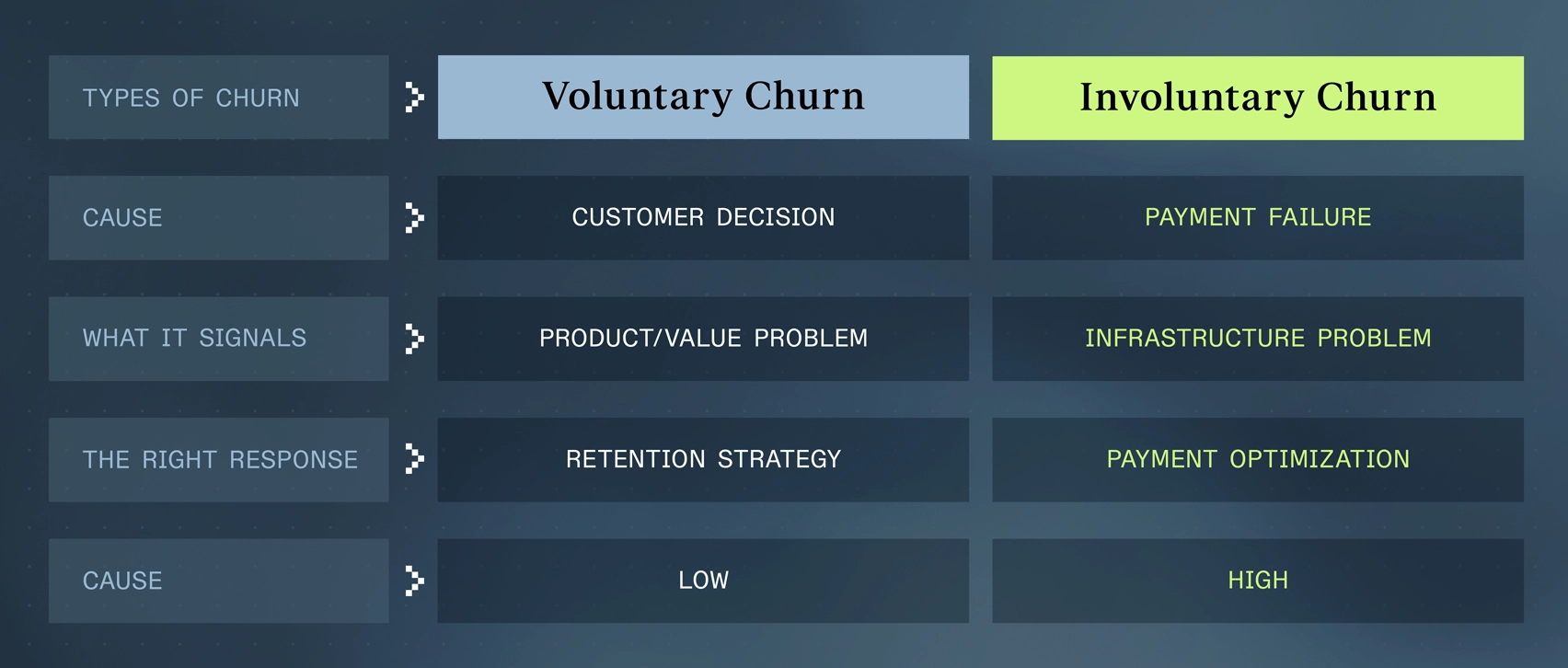

Voluntary churn is what most people picture when they hear the word churn. A customer decides your product isn't worth it anymore, so they click cancel. That cancellation is a judgement about your value proposition, your pricing, and your competitive position.

But involuntary churn is entirely different. It happens when a card expires, when a bank flags a routine transaction for reasons that have nothing to do with the customer's intent, or when a billing address no longer matches the one on file after a move or a card replacement. The payment fails, the subscription lapses, and a customer who had every intention of staying is simply gone.

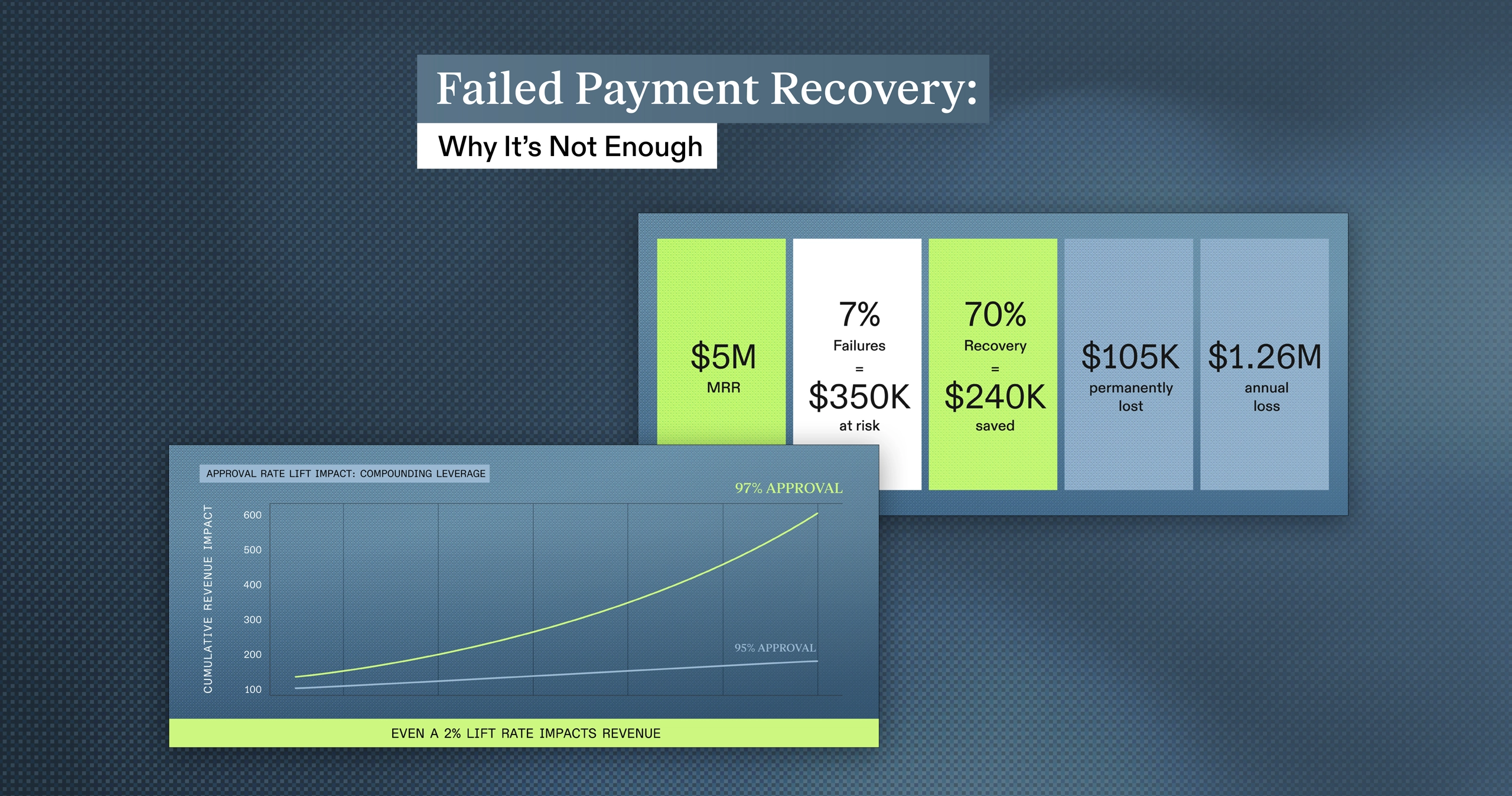

Research consistently puts involuntary churn at 20 to 40% of total churn across subscription businesses. Our own data (from when we were known as FlexPay), shows that involuntary churn caused by failed payments accounts for approximately 50% of total customer churn — yet our research finds that only 53% of subscription companies track involuntary churn.

This isn't a niche accounting problem. It's one of the most expensive misdiagnoses in subscription businesses and it's hiding inside the metric you look at every week.

A customer who cancels because your product doesn't fit their needs and a customer whose payment failed without warning look identical in your reporting. They are not the same problem.

What Misdiagnosing Involuntary Churn Actually Costs You

Here's where it gets expensive. When you misread involuntary churn as voluntary churn, you respond with the wrong approach. You invest in customer success headcount to improve the customer experience for people who already liked your product and didn't intend to leave. You build win-back sequences for customers who didn't consciously make a decision to go. You brief the product team on perceived gaps that don't exist.

The actual problem is something completely different. It's how the payments system declines a transaction when a card expires, a credit card is maxed out, or a bank applies a new rule. This involuntary churn is lumped in with your total churn amount, and it doesn't get the attention it needs. And worst of all, our data shows that 27% of consumers are likely to cancel their subscriptions if they experience service interruptions due to failed payments.

The misdiagnosis doesn't just waste resources, it compounds your financial pain because you're not just losing revenue — every month that involuntary churn runs unaddressed, you're losing the lifetime value you were counting on for long term success.

How to Separate Voluntary and Involuntary Churn

When you split your churn into voluntary and involuntary, you see two very different sides of your business.

The voluntary side tells you a story about fit, value, and experience. You can segment it by cohort, by plan, by onboarding path. You can run surveys, analyze product usage before cancellation, and build a retention program that addresses why people are leaving.

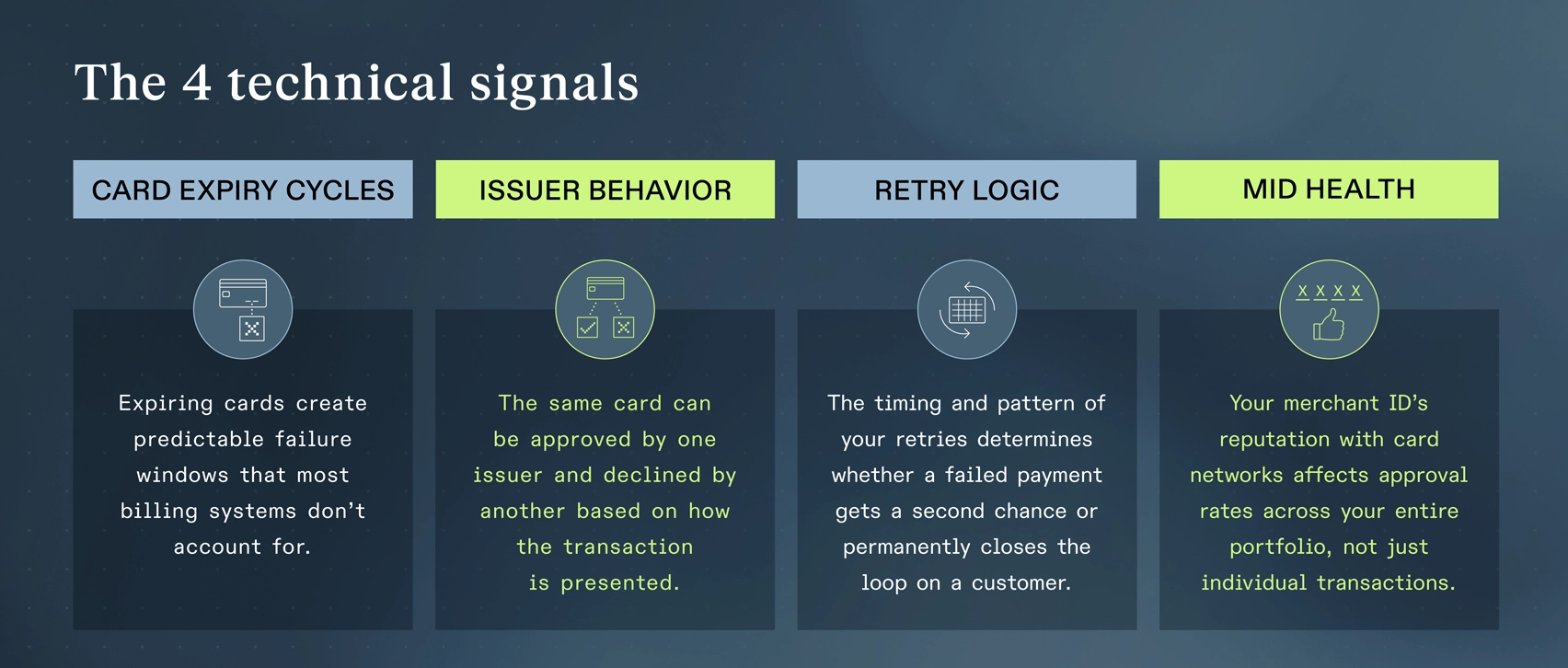

The involuntary side tells you a different story and it's worth understanding the technical signals that define it.

Together, these signals tell you whether you're looking at a payment infrastructure problem or a customer satisfaction problem, and the fix for each is entirely different

Once you can see the split clearly, you stop over-investing in product retention for a segment that doesn't need it and start applying decline recovery, intelligent retry logic, and issuer intelligence to the segment that does. The recovery rates are dramatically higher because these customers didn't choose to leave — their payment failed, and resolving the failure brings them back

Involuntary churners didn't make a decision. They were disconnected without wanting to be. That distinction matters enormously for how you approach recovery — and how likely you are to succeed.

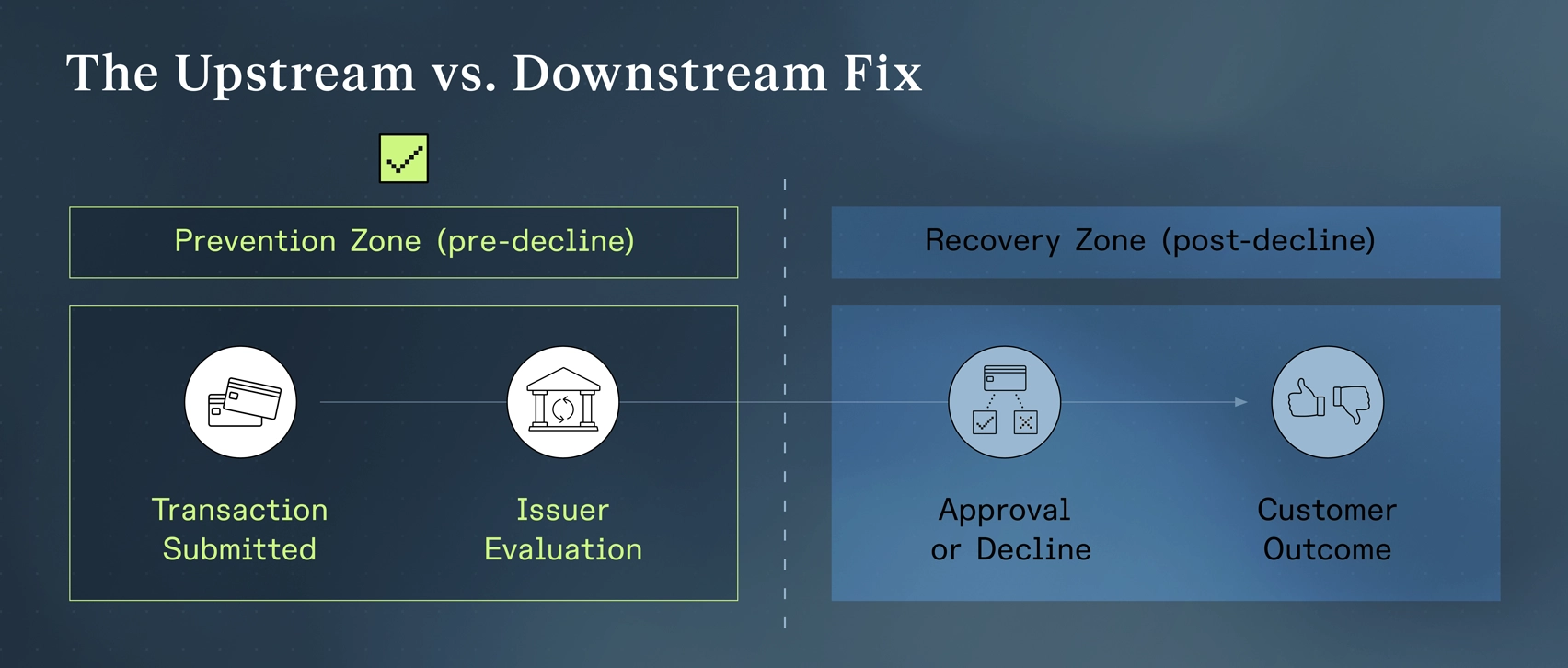

The Fix Isn't Retention Strategy. It's Prevention.

Voluntary churn is fought downstream. By the time you're intervening, your customer has already decided to leave. You can offer discounts, surface alternatives, smooth the cancellation flow, but you're negotiating against a decision that's already been made.

Involuntary churn doesn't work that way; a customer whose payment failed didn't choose to leave. The problem happened upstream in the payment flow, and that's where you need to solve it.

Prevention means going further upstream than most teams ever look. It starts with understanding how individual issuers actually behave because issuers don't all evaluate transactions the same way, and a payment that clears easily with one issuer can fail consistently with another based on how the transaction is structured and presented.

It starts with understanding how individual issuers actually behave. They don't all evaluate transactions the same way — a payment that clears easily with one can fail consistently with another based on how the transaction is structured and presented.

It means building retry logic around real decline data. Knowing which decline codes signal a temporary hold versus a hard block changes everything about when and how you retry. Without that distinction, you're hammering the same transaction pattern into the same wall.

It means routing transactions based on issuer patterns so each payment takes the path most likely to approve, rather than defaulting to a single processor regardless of outcome history.

And it means auditing the full payment flow: how transaction data is being passed, whether your MID health is working for you or against you, and whether the signals your payments send to card networks are building trust or quietly eroding it.

The goal isn't recovering customers after the damage is done. It's making sure there's no damage to recover from.

So how do you prevent payment failures from happening?

The answer is upstream intelligence.

Most payment optimization tools work from the outside in. They see a decline, apply a retry rule, and hope the next attempt lands. But that's still recovery logic, reacting to a failure that already happened.

Revaly works differently. As a Payment Performance Management platform, Revaly has direct relationships with issuing banks — the institutions making the approve/decline decision in real time. That means access to signals that never reach your billing system: issuer-level behavioral patterns, approval likelihood by transaction profile, and the friction points causing legitimate payments to fail before they ever get a chance.

That upstream access is what makes prevention possible. Revaly routes, structures, and presents transactions in ways issuers are more likely to approve, reduces false declines, protects MID health at the portfolio level, and times retries based on real decline intelligence rather than arbitrary schedules.

The result: higher first-attempt approval rates, fewer lapsed subscriptions, and involuntary churn that shrinks instead of accumulates.

When you see the share of your churn that was preventable all along, the math shifts from retention spend to revenue infrastructure and it gets compelling fast.

Want to see what's hiding in your churn number?

Get a free payment performance assessment from Revaly to find out how much of your churn is actually preventable. Contact us to get started.