Payment failures aren’t new. but the scale and complexity of declined transactions in 2026 is unlike anything merchants have dealt with before. With more ecommerce, more cross-border activity, more virtual cards, and a surge in subscriptions, legitimate customers are being denied at the moment of purchase for reasons that have nothing to do with fraud or available funds. In fact, according to PYMNTS.com, 56% of US consumers experienced a false decline in the last 90 days.

Most merchants assume a failure is because the customer entered their card incorrectly or didn’t have enough credit left on their card. But today, many valid payments fail due to hidden technical issues, mismatched metadata, conservative issuer logic, and infrastructure limitations that merchants can’t see.

Keep reading as we break down the real causes behind declined transactions in 2026 — and provide steps any merchant can take to improve payment approval rates, reduce needless churn, and prevent subscription payment declines.

Issuer Risk Models Have Become More Conservative

What’s happening

Banks have always been cautious. And rightly so—they have a huge responsibility. Banks process enormous transaction volumes, and increased fraud pressure has made issuers much more cautious. In the U.S., the FTC reported over $12.5 billion in losses from fraud in 2024, but it’s important to note that reported numbers are often a fraction of the actual total, as many cases go unreported. As a result, legitimate transactions often get included in overly strict risk models.

Examples include:

- new or unfamiliar devices

- unusual IP addresses

- inconsistent customer metadata

- device fingerprint mismatch

- tokenization inconsistencies

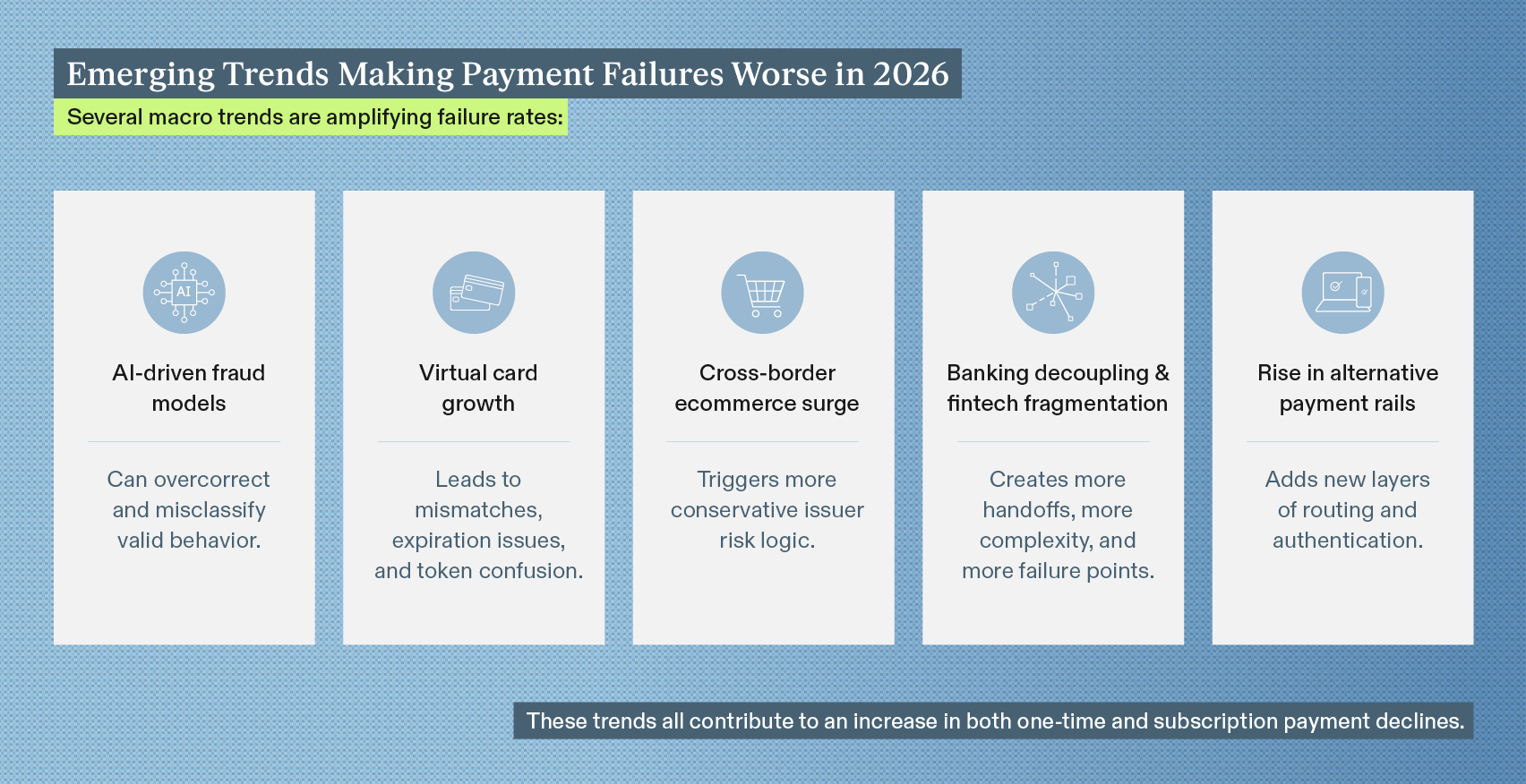

As AI-driven fraud models mature, they sometimes overcorrect and misclassify valid customer activity as high-risk. This directly contributes to rising declined transactions across ecommerce and subscription billing.

Why it matters

When issuers tighten their risk models, merchants feel the impact immediately. Every time a legitimate transaction gets mislabeled as high-risk, it triggers a declined transaction that damages the customer relationship. In ecommerce and subscription billing, this creates a domino effect: more involuntary churn, higher support volume, frustrated customers who don’t understand why their card “stopped working,” and revenue that never should have been lost in the first place. As these models grow increasingly complex — especially with AI-driven scoring — merchants without strong data hygiene or issuer-aligned payment logic fall further behind. Understanding this shift isn’t just technical context—it’s a direct signal that merchants must optimize how they format, route, and present transactions if they want to protect revenue and preserve customer trust.

What merchants can do

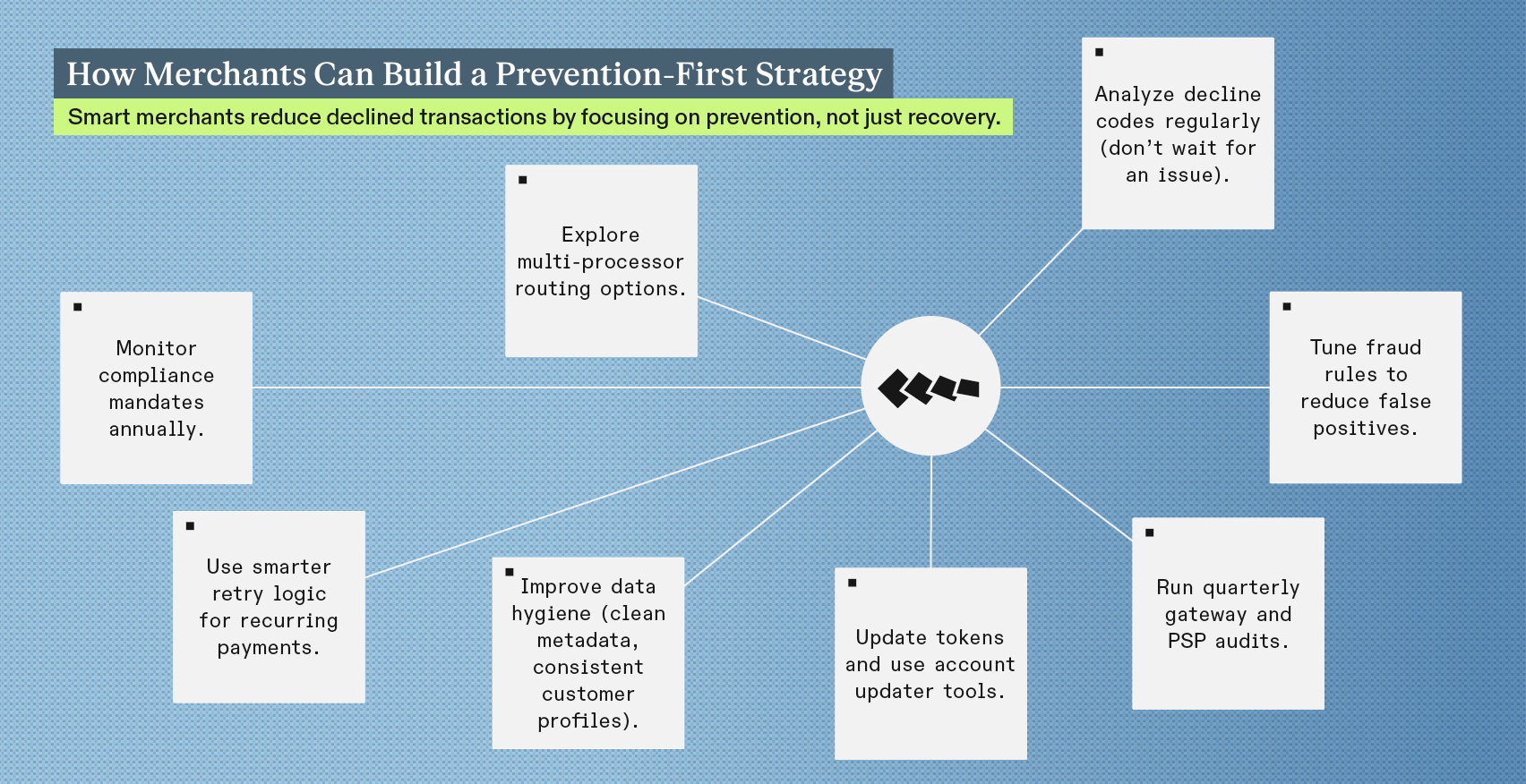

- Pass clean, complete metadata (email, address, device info, customer profile).

- Ensure tokenization and token refresh logic are implemented correctly.

- Avoid vague billing descriptors that customers don’t recognize.

- Work with partners that maintain strong issuer relationships.

These steps reduce unnecessary risk flags, especially for recurring and subscription payment declines.

Incorrect or Inconsistent Payment Request Formatting

What’s happening

A surprising number of declined transactions occur before issuer risk even comes into play. Invalid or inconsistent formatting can trigger an automatic “do not honor” or decline.

Common formatting failures include:

- missing CVV or AVS data

- incorrect currency codes

- wrong or outdated country fields

- improper 3DS/SCA metadata

- outdated BIN tables

- incorrectly formatted cross-border details

These errors are invisible to most merchants — but they create predictable patterns of transaction failures.

Why it matters

When payment requests are formatted incorrectly, issuers often decline them automatically—before risk models, fraud checks, or customer history are even considered. These failures are entirely preventable, yet they create a steady stream of unnecessary declined transactions that chip away at approval rates. For subscription businesses, formatting mistakes can break otherwise healthy recurring billing cycles, driving avoidable involuntary churn. At scale, these small technical inconsistencies turn into real revenue loss, higher support volumes, and frustrated customers who believe their card is the problem when the real issue is upstream. Ensuring formatting accuracy is one of the most impactful steps merchants can take to protect payment performance and reduce subscription payment declines.

What merchants can do

- Work with gateways to perform regular formatting audits.

- Follow network guidelines (Visa, Mastercard) for region-specific formatting.

- Clean up token data to reduce mismatches.

- Keep your integration documentation current.

This prevents a large share of avoidable declined transactions.

Static or Suboptimal Routing Paths

What’s happening

Payment routing used to be “set it and forget it.” But these days, static routing is a major contributor to declined transactions because approval rates vary significantly depending on:

- processor performance

- card type

- issuing region

- time of day

- domestic vs cross-border flows

If merchants don’t adjust routing dynamically, transactions hit lower-performing endpoints and fail unnecessarily.

Why it matters

Routing has a direct and immediate impact on revenue. Even a small gap in processor-level approval rates can translate into millions in lost renewals, involuntary churn, and customer support volume. Static routing also prevents merchants from adapting to real-time ecosystem changes—such as issuer outages, regional slowdowns, or processor-specific formatting quirks that affect why valid payments are declined. Without dynamic routing, businesses absorb performance fluctuations rather than avoiding them, making declined transactions feel random when they’re actually predictable and preventable.

What merchants can do

- Benchmark approval rate performance across processors quarterly.

- Avoid lowest-cost routing when it sacrifices approval performance.

- Use multi-processor strategies when possible.

- Consider a Payment Service Provider (PSP) that uses intelligent routing capabilities.

Optimized routing is especially important for subscription payment declines where recurring patterns are sensitive to processor behavior.

Compliance Mandates Are Adding New Friction

What’s happening

2026 will be a high-friction year for compliance. Global and regional mandates continue to evolve, including:

- Visa Acquirer Monitoring Program (VAMP)

- Strong Customer Authentication (SCA) and new European exemptions

- 3DS2 metadata requirements

- Network tokenization enforcement

If merchants don’t pass the right compliance signals or updated metadata, issuers often default to decline — even when the transaction is legitimate.

Why it matters

Compliance is no longer a simple checkbox — it directly affects whether a valid payment gets approved. When required authentication fields, token rules, or network-mandated indicators are missing, issuers often treat the transaction as high-risk by default. That leads to unnecessary declined transactions, especially in subscription payment declines where the customer never interacts with the checkout experience.

As compliance rules get stricter each year, merchants that don’t stay aligned with the latest network, issuer, and regional requirements see a measurable hit to revenue, authorization rates, and customer trust. Staying compliant isn’t just about avoiding penalties — it’s about keeping legitimate customers from being declined for technical reasons they’ll never see.

What merchants can do

- Monitor Visa, Mastercard, EMVCo updates quarterly.

- Validate metadata when new mandates go live.

- Test authentication flows across regions.

- Ensure all SCA/3DS2 indicators are properly set.

This reduces compliance-related declined transactions.

High Fraud Noise Is Creating More False Positives

What’s happening

Fraud attempts continue to rise, with 48% of Americans reporting that online hackers made fraudulent charges on their credit or debit card. This rate of fraud makes risk models hypersensitive and good customers often look suspicious.

Triggers for false positives include:

- VPN usage

- shared Wi-Fi or public networks

- cross-border location mismatches

- sudden changes in purchase velocity

- rigid merchant-side fraud filters

The result is a higher rate of false declines when valid customers wrongly rejected.

Why it matters

When fraud creeps into the system, issuers adopt aggressive risk thresholds, which directly increases declined transactions—even for loyal, returning customers. For subscription businesses, these false positives compound into avoidable subscription payment declines that frustrate users and cause involuntary churn. The reputational impact is also significant: a false decline feels like a broken user experience, not a fraud safeguard. Every time a legitimate customer is rejected, trust is diminished and the likelihood of cancellation rises. Reducing false positives is essential for preserving revenue, customer loyalty, and long-term LTV.

What merchants can do

- Tune fraud rules regularly (not just once).

- Use behavioral analytics rather than simple rule-based filters.

- Avoid stacking multiple fraud tools that conflict.

- Provide issuers with cleaner fraud signals to reduce misclassification.

This can dramatically reduce declined transactions and false-positive rates.

Recurring Billing Has Outgrown Legacy Infrastructure

What’s happening

Subscription-based business models continue to grow, but issuers still struggle with recurring payment patterns. As a result, subscription payment declines remain one of the most common and costly payment issues.

Recurring billing fails when:

- amounts fluctuate slightly

- the card has expired or been replaced

- network tokens aren’t refreshed

- customer doesn’t recognize the descriptor

- issuer flags the attempt as unexpected

The slightest disruption in the expected pattern can trigger a decline.

Why it matters

Recurring billing is supposed to be seamless—but when issuers still depend on legacy logic, even good customers get declined. Every false decline interrupts the subscriber experience, increasing the chance that customers abandon their renewal altogether. For merchants, this means preventable revenue loss, higher support volume from confused customers, and rising involuntary churn. Because so many of these declines stem from predictable billing patterns, fixing them is one of the highest-impact ways to improve retention and protect recurring revenue. Subscription businesses that actively address these issues see dramatically higher lifetime value and far less involuntary churn caused by payment failures.

What merchants can do

- Use clear, consistent billing descriptors.

- Activate account updater and token refresh tools.

- Provide customers with advance renewal notifications.

- Build smarter retry strategies (timing matters).

- Encourage secondary payment methods for high-value subscriptions.

These changes directly reduce subscription payment declines and the involuntary churn that does along with them. Our study with PYMNTS (when we were known as FlexPay) showed that 27% of consumer who experienced a false decline let their subscription end or switched to competitors as a result.

Data Silos Prevent Root-Cause Diagnosis

What’s happening

Merchants often don’t know why a transaction was declined because the critical data lives in separate systems. This date includes:

- gateway logs

- fraud tool decisions

- processor decline codes

- issuer error messages

- CRM customer history

With no unified view, payment teams rely on assumptions instead of insight — leading to recurring issues with declined transactions and repeat failures.

Why it matters

When merchants can’t easily connect the dots between gateway behavior, fraud decisions, processor codes, and issuer responses, they lose the ability to diagnose why valid payments are declined. That lack of clarity leads to recurring declined transactions, higher subscription payment declines, and ongoing revenue leakage that could otherwise be prevented. Without unified data, teams end up treating symptoms instead of solving the true cause—resulting in wasted operational effort, rising support tickets, and avoidable customer churn. Centralized intelligence turns payment failures from guesswork into solvable problems, allowing merchants to improve approval rates with precision rather than trial-and-error.

What merchants can do

- Centralize reporting across gateway, PSP, and fraud tools.

- Pair decline codes with customer behavior for context.

- Review failure patterns monthly or quarterly.

- Push for higher transparency from processors and acquirers.

Better visibility = higher approval rates.

A prevention-first mindset dramatically reduces subscription payment declines and improves lifetime value.

Valid payments will continue to fail in 2026, not because customers are untrustworthy, but because the payments ecosystem has become more complex, fragmented, and sensitive to even the smallest inconsistencies. The merchants who protect revenue most effectively will be those who treat payments as a performance discipline — strengthening data quality, tuning fraud and routing strategies, aligning with evolving compliance standards, and proactively managing approval health across their entire payment stack.

How Revaly Helps Merchants Fix Declined Transactions at the Source

Valid payments will continue to fail in 2026 — not because customers are unreliable, but because the payments ecosystem has become more fragmented, more regulated, and far less forgiving of even tiny inconsistencies. The good news is that these failures are both measurable and fixable when merchants take a performance-focused approach. Revaly was purpose-built to help businesses do exactly that with exclusive issuer and network intelligence no one else can access.

With Revaly, merchants can:

- Eliminate preventable declines through intelligent gateway formatting, data optimization, and issuer-aligned payment structure

- Reduce false positives by providing issuers with cleaner fraud signals to reduce misclassification

- Improve recurring billing performance with smarter retries, token management, and descriptor consistency

- Route transactions more intelligently using real-time insights

- Break down data silos with unified reporting and multi-layer payment intelligence

- Stay ahead of compliance changes with continuously updated mandate logic baked into the platform

Revaly helps merchants move from reactive firefighting to proactive payment performance — ensuring more valid payments succeed, more subscribers remain active, and more revenue is received as expected.

If you want to learn more about how you can improve approval rates, reach out to the Revaly sales team and let’s have a conversation.